I wanted to say thanks to everyone that is trying to dumb this down for me, it really helps and I appreciate it.

I also wanted to apologize if I triggered anyone about the “life insurance” thing. I should have probably left that out. Where I am from we get raised massively different. Doesn’t make it right, its quite the opposite. I’m sorry if that was hard on anyone. Thats my fault.

On another note, I am ticked off at the prior generation of my family for a brand new let down. Thanks, internet. I know I grew up different than most, but sometimes it smacks you right in the face unexpectly on a Thursday.

The good news is that it really doesn’t have to be complicated. Budgets can be easy things to work with, as long as you keep at it and make it a habit.

You know how much you’re making. You know how much you’re spending. To save $7,500-12,000 a year, you either need to make more money or spend less money. That’s the hard part.

How much you need in retirement is going to be based on how you live now and how you want to live in retirement. A couple with two six figure incomes that wants to continue the same lifestyle will need more money than a couple that earns $ 75K total and plans to retire to Thailand.

But something I don’t think I saw anyone mention - contributing $1000 to a tax deferred retirement account doesn’t actually cost $1000 because of the taxes you won’t pay. The website for my account had place where you could enter a contribution amount and it would tell you how much your net pay would change.

Are you sure it’s Fidelity Investments that you are dealing with at your job? because everything you have been saying about them from what the Fidelity advisor told you in 2009 to how that “401K” they supposedly manage for the company you work for, is almost 180 degrees opposite of how they actually work. There’s something seriously off about this story.

I just want to say that my hat is off to your for asking the questions so articulately and patiently! I wish you and the Mrs. all the best.

Maybe some of the very smart/well-informed people here can give you some tips about how to find and vet a “financial advisor.” I and others I know have had bad experiences, especially with companies who have products to sell (lookin’ at you J.P. Morgan ). OTOH others I know have had bad luck with independent advisors. When you don’t understand this stuff, it’s hard to know if you’re being treated right or not.

It sometimes feels as if life happens suddenly, indeed. The good news is that you still have time to plan for retirement. You posted above that you’re 40, so that’s still a decent amount of time to save and realize growth before retiring. Assuming a retirement at 62 (a typical benchmark), you’ve got 22 years to invest and plan.

And importantly, as @Munch pointed out, you can expect growth of your investments over time; you might be surprised at how much. There are many online calculators you can use to estimate it. The key is to maximize the time value of money by investing early to take advantage of the compounding interest. Here’s one that also offers other tools, like vetting financial advisors:

A quick online search shows that there are a number of banks with ‘Fidelity’ in their names, located and headquartered in different states. These banks, which are independent of each other, should not be confused with Fidelity Iinvestments, which is one of the largest investment firms in the USA, and probably the world. It’s certainly possible that you are in communication with two totally different entities.

Whoever this guy worked for, he should have been fired years ago. I find it hard to believe that anybody employed by Fidelity Investments would say this. Do you happen to have the guy’s contact info and/or business card?

I can only echo what others have said in this thread: talk to somebody in your HR or payroll department about your situation, or seek financial advice elsewhere. I wish you luck.

This. Whereas a pension is considered a “defined benefit” plan (because you know ahead of time how much your pension will be), a 401(k) is a “defined contribution” plan (because you know what you’re putting into your 401(k), but you won’t know how big the final balance will be until you actually get to retirement age).

For most folks, their annual income during retirement (from SS and from things like 401(k) withdrawals) tends to be less than what they were earning during their working years, so they end up in a lower tax bracket. By putting money into your 401K while you’re earing a high salary, you protect that money from taxation until after you retire - at which point it’ll probably be taxed at a lower rate, saving you some money. IOW, if you’re trying to save money for retirement, you can reduce your tax bill by putting that money into a tax-deferred account (like a 401(k)).

401(k) accounts also have special requirements for taking money out. You can withdraw from your account after age 59.5 without any penalty (but you’ll of course pay income tax on that withdrawal). withdrawals before that age are severely restricted, and in many cases get hit with a 10% penalty (on top of the income tax). This is to discourage workers from casually taking money out of an account that they are supposed to be saving for retirement. Some exceptions are allowed, e.g. particular cases of hardship, or also loans (the latter must be paid back at a later date).

Some employers match their employees’ 401(k) contributions to a certain percentage of the employee’s salary, but some don’t. a 5% match is common; some employers will match to 10%. If an employer is offering a match, then an employee who doesn’t contribute enough to their 401(k) account to get all of that match is missing out on free money. Even after you think you’ve got enough money in your account, you shouldn’t zero out your contribution; you should only dial it back to the minimum amount that will still get you that match.

The IRS places a limit on how much you can contribute to a 401(k) each year. For 2024, the limit is $23,000. So for example, suppose you’re earning $75,000 a year at a company that offers a 5% match. You’re allowed to contribute as much as $23,000 per year from your own paycheck to your 401(k), and your employer will kick in 0.05 * 75,000 = $3750. If you don’t contribute anything, your employer won’t either.

401(k) accounts are a fairly common thing in the corporate world. People working in academia typically have access to 403(b) accounts instead; these are basically the same thing, just a different name. US federal government employees have the Thrift Savings Plan (TSP), which has the same sort of rules as 401(k) and 403(b) accounts.

If you’re that young, then time is still on your side. If you can work and save for the next 30 years, you can be in pretty good financial shape for retirement.

It can’t hurt to talk to someone. If you’re concerned about whether they’re advising in your best interests, make a note of what they tell you and bring it back here for discussion.

It’s scary that this would be common anywhere. Not only do you end up sacrificing the final decades of your life, but you spend your working years thinking about the necessity of offing yourself when your career ends. That sounds like an awful way to live.

The amount you need to retire depends on how much you want to spend each year during your retirement. How much will that be? Probably a little less than you’re spending right now. There are retirement calculators out there that can provide a coarse estimate what you need. Here’s one from NerdWallet:

You don’t mention your salary, so I tried an annual pre-tax income of $50,000, and a retirement budget of 70% of pre-retirement income ($2151/month). I also assumed a $12,000/yr social security benefit, so I put $1000/month in the “other retirement income” box. With all that, it looks someone in that situation would need to contribute about $570 per month into their retirement account starting at age 40. You can go there and put in your own real numbers and see what you get; there are boxes to the left of the plot where you can type in numbers, and there are also sliders below the plot that you can move to adjust things.

If you haven’t been getting annual reports from the Social Security Administration in the mail, you can go sign up here for an online account that lets you access the same info that would have been in those reports. That includes a record of all of the income that you’ve earned (at least according to the tax returns you’ve been filing), and an estimate of what your annual SS benefit will be after you retire.

As you might expect, simple calculators like the one at NerdWallet make a lot of assumptions. If you click on the “Advanced Details” below the “other retirement income” box, you can see and adjust some of those assumptions. They’re assuming a pretty reasonable rate of return on your investments, 6%. And you will have to invest a significant portion of your nest egg in equities (stocks), not just bonds in order to achieve that. Some mutual funds offered in your 401(k) plan will be composed exclusively of stocks, some will be 100% bonds, and some “life cycle” mutual funds feature a blend of the two that slowly changes so that they contain more bonds and less stocks by the time you retire. A financial advisor can make suggestions in this area - and as I said earlier, we’ll all be happy to comment on whatever such an advisor tells you.

Those sound like certificates of deposit (CDs). Usually when you deposit money in a checking or savings account at a bank, you earn a tiny amount of interest for letting the bank use your money while you aren’t using it. But your account balance can go up or down unpredictably based on your deposits and withdrawals, so banks won’t pay you a ton of interest. To get a higher rate, you can promise the bank that they can use a chunk of your money for an agreed-upon period of time. That’s a CD, and instead of earning a fraction of a percent per year in interest, they typically earn several percent. Banks offer CDs with periods ranging from a few months to several years. At the end of the agreed-upon period, you can withdraw your money (along with whatever interest it has earned), or keep it in there for another round.

Having money in CDs tends to be better than having it in a savings account (in terms of how much it earns), it’s rare to find a CD that pays more than inflation. If you put your money in CDs, it will accumulate and generally maintain its purchasing power, but it won’t really grow (i.e. you won’t be able to buy more things later with it than you can right now). For real growth, you will need to put some of your money in mutual funds that contain stocks. Consider the difference:

if you put $10,000 into a CD 30 years ago and earned 4% per year on it. It would now be worth about $32,400.

if you put $10,000 into a mutual fund that tracks the S&P500 stock index, it would now be worth $191,344.

This. Fidelity is not a bullshit fly-by-night operation; they are a major financial company that’s been around for about 80 years now. My wife has a lot of her 403(b) money in their accounts, and together we also have substantial ordinary investments with them. If there is any kind of fraud going on, it’s almost certainly not by them.

Since we are explaining the basics I figured, let’s not assume anything, and talk about why a 401k is so beneficial (compared to investing the money in most other places, or putting it in a mattresses or something). I’ve found that people often don’t really know the basics, so reviewing them can be helpful.

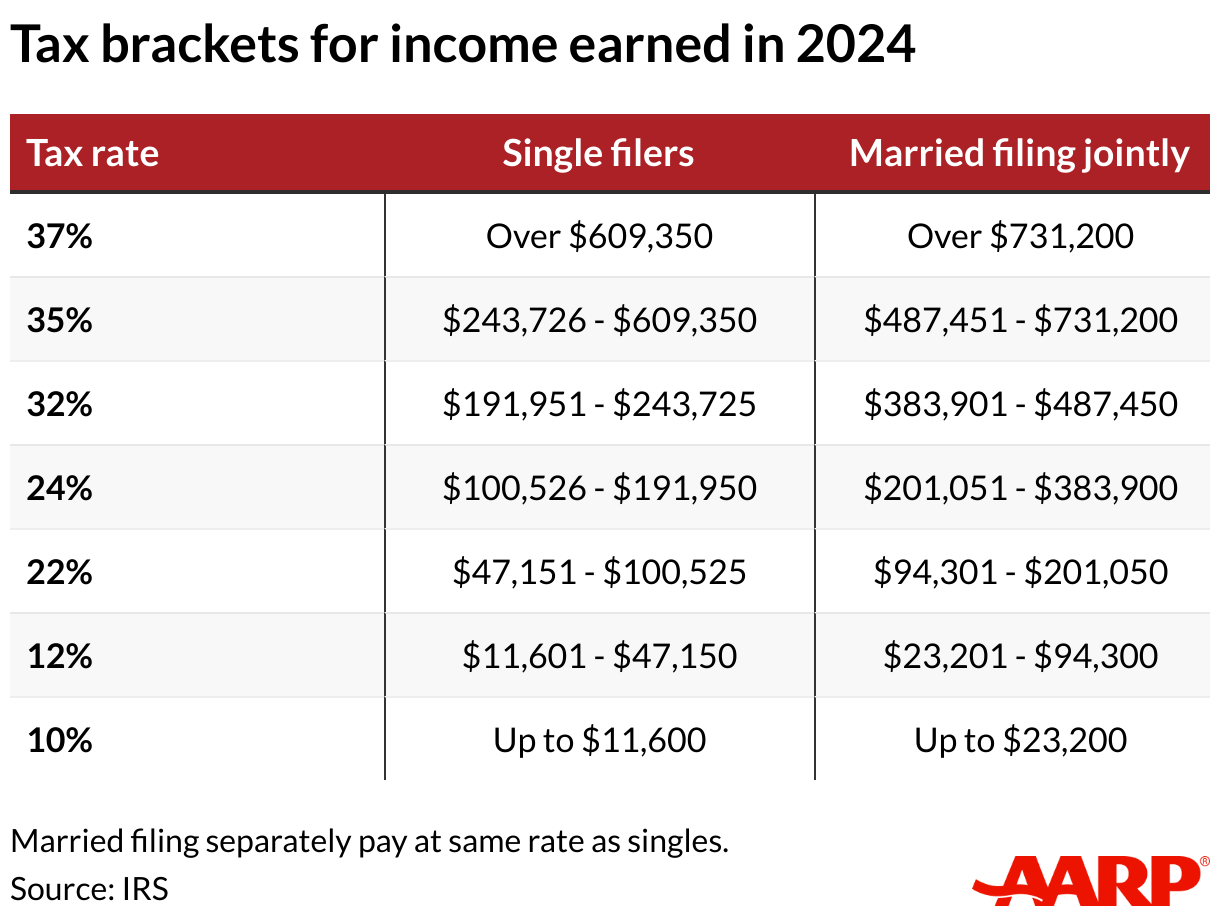

You probably know about tax brackets. The more money you make, the more money you pay in taxes.

However (and this is something that confuses even some of my coworkers in the financial industry at times) you only pay the higher rate on income that falls in the higher tax bracket.

Here are the tax brackets for this year.

If you make $50,000 a year, you may say “I pay 22% of my income in taxes”, because that is the bracket you fall into. But that’s not quite right, because when you get a raise from $47,000 to $50,000 you only pay 22% on the last $2,850 - the rest of the money is still taxed at 10% (the first 11,599) or 12% (the other 35,550).

[I work in the financial industry, my job at the time involved tax brackets, and yet I have a distinct memory of one of my coworkers complaining that a raise put him into a higher tax bracket meaning he would be taking home less money each year. So I would not assume that lay people understand this information ]

That brings us back to the 401k. In our scenario above, you could put that 2,850* into a 401k account. Others have mentioned ghat your taxes are “deferred”. This means you put the entire 2,850 into the account, without paying any taxes. The money still gets taxed eventually - when you remove it from your account - but the benefit there is if you expect to make less money when you are retired than when you are working (which is true for most people who don’t have some serious investment portfolios or real estate or something), that money will be falling in a lower tax bracket when you finally do use it.

Another benefit is that the 401k account doesn’t just sit around; it gets invested. Typically, if you let someone like Fidelity manage your money, what they offer is a series of packages that split your money between safer and riskier investments. “Riskier” here means that they are more likely to move (up or down) with the market. So the recommendation is, the younger you are, the higher the portion of your savings that should be in investments that swing with the market, because even if a dip happens you’ll have plenty of years to make up that ground befoe you retire; but as you age, you switch to more conservative investments, that won’t grow as much in a healthy market but won’t drop as much in a crash, either.

So the fact that you delay paying taxes on that money means the portion you’ll eventually pay as tax gets to grow for you in the meantime, earning you even more interest.

*it’s actually a bit more complicated with deductions and credits and such but we can ignore that for now

I was just offered a job that gives no 401k matching whatsoever. Under such circumstances, am I better off putting $6,500 (the legal maximum) out of my own pocket into my Roth IRA every year? As I understand it, it only makes sense to put personal money into an IRA but not into a 401k, since 401k is treated as pre-tax but the Roth is post-tax.

@Velocity It depends on several considerations, including whether you anticipate being in a higher or lower tax bracket when you begin withdrawing from the account. Many people anticipate lower income during retirement (and thus a lower tax rate), so it makes sense to defer taxes via a 401k or traditional IRA on the theory that you will pay less in taxes. If, however, you are planning for a more lucrative retirement, it may be better to eat the taxes now rather than later.

Most 401k plans offer a Roth option these days. However, my default is typically to suggest putting it in a Roth IRA first, then your 401k. 401k plans nearly always have higher fees, and there are emergency withdrawal options in your IRA that a 401k may not have (in Roth IRAs that have been open for 5 years, you can withdraw the principal with no penalty).

I also wanted to chime in about Fidelity. My 403(b) account is managed by Fidelity, and they are wonderful to work with. Their website is easy to use, their statements are straightforward, and it’s easy to schedule one-on-one meetings with an advisor if you need more personal advice. They are a very reputable company, and I can’t imagine anyone working for them telling someone that they wouldn’t be able to retire.

I’m in somewhat the same situation as the OP, in that I was fairly far along in life before I really started paying attention to savings and retirement issues. I don’t think I was quite 40, but I was in my mid-to-late thirties. The good news is, I’m doing pretty well now. Not as well as I might have if I had started out in my twenties, but well enough that I think we will be comfortable in retirement. (It helps that my wife is a teacher, and thus has a pension).

Being 40, you still have quite a bit of time, 20 to 25 years. You’ll certainly need to be more aggressive in how much you save than if you were 22, but it’s still doable.

I have found NerdWallet, which Machine_Elf mentioned above, to be a good place to learn about finances. I also like The Money Guy Show on YouTube, but they may be a bit too esoteric for someone who’s an absolute beginner.

Kudos for folk trying to explain/advise. OP - this is going to come across as insulting when it really isn’t intended to be - but it is quite impressive that you’ve been able to make it to age 40 and remain so ignorant about finances and investing. It is not entirely your fault that your schools and family have let you down so abjectly. And perhaps it is something you’ve just never been really interested in, so you haven’t tried to educate yourself. I can relate - I really dislike managing money. So I chose to pay a guy to manage it for me. Folk will claim it isn’t worth it, but he’s done well by me, and I put a high value on not having to fuck with it myself.

But I’ll suggest you may want to take it upon yourself to educate yourself and develop some good habits at this point. The folk around here are quite intelligent and well intentioned, but you might just want to kinda make it your hobby for the immediate future to improve your financial knowledge. There are any number of books/websites sich as “Investing for Dummies.” You don’t have to become an expert, but you DO need to build up a basic vocabulary and understanding of basic concepts. Look for free workshops at your local library or basic classes at a community college.

Good luck. As others have suggested, it need not be exactly rocket science. Can be as simple as investing in indexed funds and periodically rebalancing your investments (which you need to learn what those are.) Just pick a couple of funds with Vanguard or Fidelity, keep adding cash and pretty much let them be. Also, you need to get a handle on your income/assets/liabilities, and develop healthy financial habits. Not terribly complicated. You are getting a later start than most, but some folk never get to the point of realizing there is something they need to know.

A 401(k) is a plan that many (most?) companies sponsor for their employees, to encourage retirement savings. Some nonprofits and public sector employers have similar programs, just called something different (e.g. the Federal government’s Thrift Savings Plan).

In our parents’ day, you’d work for the same company for 40 years, then retire with a pension that was entirely funded by the company. That was typically a “defined benefit” plan, where they calculated a figure based on your average earnings and years of service. Those are nearly extinct these days, except for public sector jobs.

If a company has a 401(k), they’ve usually used that to replace the old defined benefit plan. The idea is, you put aside x% of your money, and the company “matches”. Typically a cap of 3% of your income. So if you earn 100,000 a year, and put aside 10%, the company also contributes 3% - so you’re actually saving 13% a year. The catch is you have to work for the company a certain length of time (up to 7 years, depending on the plan) to be entitled to all of the company’s money if you leave. This kind of plan is called a Defined Contribution plan.

It’s a great deal for the company, because a) they only put in that full 3% (or whatever) if YOU put in enough to get the matching, b) if you leave early, they get it back, and c) the company is no longer at risk of needing to fund a defined benefit pension: once their money goes into your account, they don’t have to worry about it any more - it’s YOUR responsibility to manage the investments.

As far as amount to retire: that varies based on what your expenses are. And don’t forget, the amount you put aside every year will earn income.

I plugged the figure you mention (46667) into Excel and assumed 3% annual return, and you hit the 1.4 million mark about age 61, with that growth. Now, that’s a very ambitious amount to contribute every year (my husband and I don’t do that much and we’re relatively high income), but putting ANYTHING aside will be better than nothing.

I’d say you should look HARD at the company’s current 401(k) plan and find out what the deal is. Who manages the plan (e.g. Fidelity, Vanguard etc. or Billy Bob’s Brokerage House where Billy Bob is the owner’s brother-in-law). What are the investment options, for example. And when are company matching contributions sent to the investment company.

Fidelity ought to be able to look your info up based on the letter you got, at least. They are, by and large, not hinky at all, so the only thing I can think of that explains what you have said is that the earlier plan was only allowing the investments to be made in the company stock.

One rule of thumb is that in retirement, you need to be able to replace 80 to 100% of your working-life income. 80% is the general advice, but some advisors say to aim for closer to 100% if you plan on doing stuff like travelling. And there are a lot of factors like expected housing expenses (we personally are talking about downsizing to something smaller / cheaper), moving to a cheaper area of the country, and so on. And don’t forget your Social Security benefit. Who knows how things will change in 20 years, but for now, you can at least look at your SSA account online for estimates.

Looking at some made-up numbers: Let’s say you and your wife are pulling in 80,000 a year. 80% of that is 64,000, or 5333 a month. And let’s say your SS benefit would total 3,000 a month. So you need to come up with 2,333, or 28,000 a year from your investments.

Another rule of thumb is that you should be able to draw down roughly 4% (some more conservative estimates say 3%) of your retirement account every year. 28,000 is 3% of 933,333 dollars. At a 4% drawdown, that’s 700,000 dollars.

In your specific situation: from what you’ve said, you’ve paid down a boatload of debt (YAY YOU!!!) and your housing expenses are a lot lower. Can you manage to save half of that savings, somewhere? If you truly are not sure about the company’s 401(k), then save as much as you can in an IRA. That’ll be less than you can put aside in a 401(k) (5,000 versus 15,000 or so, and I’m quite certain those limits are not correct, but you get the picture). But ANYTHING is better than nothing.

And, do Roth versus traditional if you can. Roth IRAs don’t save you any money on your income taxes this year, but you NEVER PAY TAXES on the growth. A traditional IRA, you deduct the contributions this year (barring some limits on income and availablity of a workplace plan), but you pay taxes when you withdraw the money. Also, with a Roth IRA, you can access the contributions (but not the growth) after a certain period of time, in an emergency; but don’t do that.

The catch there is that depending on your income, you may not be eligible for a Roth IRA (we are not; I suspect the OP would be). And of course the 401(k) has much higher contribution limits.

You can borrow against your 401(k) in an emergency, at a very low rate (we’ve done it a couple times). There’s usually a small setup fee, and the repayments are taken from your paycheck with interest - but you pay that interest to YOURSELF. If you leave your job, you have a short time to repay it or it’s treated as a distribution, with taxes and penalties, so it’s not a risk-free option, but it is there.

One general guidance for how to invest spare money, that I think I read here first:

Put enough of your income into the 401(k) to get the full company matching (otherwise you’re leaving free money on the table).

Max out your IRA/Roth IRA with anything else you can afford

If you can still afford more, max out the 401(k)

And if you STILL have money to spare, put it in regular investments.

In case OP is not aware, you can put additional funds into ordinary (not tax-deferred) investments. So if you have cash left over because you’ve bumped up against a 401(k) or IRA contribution limit (or flat-out don’t trust your company’s 401(k) program), you can open up an account at Vanguard, Fidelity, T. Rowe Price, or one of many other financial service companies, and just use that spare cash to buy shares in whatever mutual fund you want. Money you deposit into ordinary investments is after-tax money - that is, you pay income taxes on it just like the money you spend on groceries or rent. The flip side is that if you’re invested for at least one year, most of what your investment earns in this type of account is taxed at the capital gains tax rate, which is typically less than the income tax rate that applies to tax-deferred accounts like 401(k). You can also withdraw your money from ordinary investments at any time (although if you withdraw after less than a year your earnings will be subjected to short-term capital gains tax, generally the same as income tax).

Hi, @Translucent_Daydream ! Sorry for getting back so late, but it looks like others have already answered your question. My company matched up to 6% of my contribution, so if I contributed 6% of my salary; my company contributed another 6%, so I had a 12% total contribution. The additional 6% was free money to me.

When I was younger, I was annoyed by people who declared confidently that retirement plans and social security “wo(uld)n’t be around” when we retired. I know that that’s a true statement in the sense that fewer companies are offering fixed benefit plans, but that was already happening, so it wasn’t news. And while some consider it a poor swap, fixed contribution plans have largely replaced pensions.

I was annoyed because it seemed such people didn’t really have much insight on the future, and were using blanket cynicism to look smarter than they were.

But this thread makes me realize that there may be a much bigger problem caused by such talk: young people may decide that if retirement plans “won’t be around” when they retire, they may opt out of contributing anything to their retirement.

Anyone who is able to contribute to their retirement and deliberately refuses to is certainly going to regret it.