I guess the other problem with cheque or electronic fraud is - how do you get the money out? (Same old money laundering problem) As long as the money is bits in the system, it can be tracked. So to run a criminal enterprise, you need a way to either withdraw cash, or send it to a country whose banks don’t cooperate with the rest of the world. Also, a decent livable income nowadays is in the order of at least, say, $50,000/year. You start trying to extract that much money from the banking system in cash, you will trigger fraud alerts all over, and likely be identified quickly, especially today when cash is less commonly used.

Frank Abagnale (Catch Me if You Can) claimed to have manufactured fake cheques and cashing them all over the USA and Europe. (although there are claims he seriously exaggerated his abilities - once a con man, always a con man) One gotcha is that in the days of less sophisticated computers, the funny numbers on cheques were printed with magnetic ink in those interesting patterns to make automated reading easier. Just printing a cheque on ordinary print-shop would fail the first test after deposit.

In Japan and Taiwan, it’s similar. People sending money need the account name and number and bank information, but you can’t pull money out with that information.

You can tranfer money online, with an app, or at the bank ATM with your cash card, or with a teller and you need to supply ID.

It used to be that if you had an inkan, the registered seal for the account, anyone could withdrawl money. Was that way people scammer the elderly? Yup. They would visit the elderly and claim to be from the bank, and borrow the seal. That has been changed.

These days, it looks like the telephone scams are more common.

When someone made fake checks with my (business) info on them and used them to steal money from me, one of the checks wasn’t signed (on the front) and I had to fight with the bank to get my money back on that one just as hard as I had to fight to get my money back on the others (which had signatures that didn’t match out signatures, even the names were different).

I couldn’t even get the bank to understand that their argument that they can’t (don’t) compare every signature on every check to the signature on file falls apart here because this check wasn’t signed in the first place. There was nothing to compare, the teller/mobile app where it was deposited or them (my bank) when it made it’s way to them, somewhere along the line that check should’ve been rejected for not being signed. I’m of the opinion that even if I was the one stealing my checks (as the bank was accusing me of), this one was still their fault.

You scam another person. It’s not much different than the craigslist overpayment scam. I forge a check for $1000 and make it out to you. I tell you to deposit it into your account, keep $100 and give me $900. If/when the account owner notices it, and I’m sure plenty don’t, they notify the bank, the bank pulls the funds out of your account and you’re out $1000 and I have $900.

These pop up semi-regularly in the news and in police reports.

I’m not saying it doesn’t happen. The problem with all this is doing it at scale. My point - someone might get away with it for a little pocket money, but many people get paid $900 a week. They would have difficulty making a living on this. Each individual scam is an opportunity to get caught. And to get untraceable cash, you still have the “send me the $900” detail. It may be gift cards, but then where it gets spent is traceable… and so on.

As I understand, Canadian eTransfer is not reversible unless it’s proven fraud as in “I didn’t send that, I was hacked”. If you sent it on your own volition, such as wrong email address or phone number, it’s on you to get it back - even if you get scammed and send the $900. You meant to send it.

You hit [send], it’s gone, and the bank’s answer to any problem is “tough luck; sucks to be you.” The banks have got a major awareness program running full tilt now about all the ways scammers can persuade you to click [send] and be screwed. Not because they’re responsible for covering your losses, but because they fear legislation might make it their problem in the future.

Well, the banks did not start out that way. They were marketing all the convenience. And it is massively convenient.

It’s when the very smart scammers met up with the very dumb Americans at scale that the banks recognized the fundamental problem: Most Americans are too stupid / careless / trusting to be left alone without adult supervision. So now they’re trying to graft (automated) adult supervision onto the system.

I knew of someone, friend of a friend, who went to jail for passing stolen cheques. He went to jail. The person he bought the stolen cheques from, stole cheques and sold them to hopeless drug addicts, who took all the risks and all the jail time.

Under Regulation E, your bank is liable for protecting you, specifically if you notify them within a timely manner that fraud has been committed against your account (60 days). This is why you should reconcile your bank account, or at a minimum review your bank statements for unknown charges or transactions.

The distinction, as I understand it, is that PayID in Australia appears to be universal (i.e., everyone uses the same system). In the U.S., we have a number of competing electronic payment systems (Zelle, Venmo, PayPal, etc.), and not everyone (or every bank) may be using the same system. Even Zelle, which was, as you note, set up by banks*, isn’t universal, and there are some U.S. banks and credit unions which don’t accept it or allow it to be used with their accounts.

*- According to Wikipedia, Zelle is co-owned by seven major banks: Bank of America, Truist, Capital One, JPMorgan Chase, PNC Bank, U.S. Bank, and Wells Fargo.

Regarding the lack in America of a truly universal electronic payment system, a recent article in the New York Times introduced me to the FedNow Service, through which “businesses and individuals can send and receive instant payments in real time, around the clock, every day of the year. Financial institutions and their service providers can use the service to provide innovative instant payment services to customers, and recipients will have full access to funds immediately, allowing for greater financial flexibility when making time-sensitive payments.”

It’s not universal yet but perhaps with the sponsorship of the Federal Reserve, it can become one. That would be great if it happens.

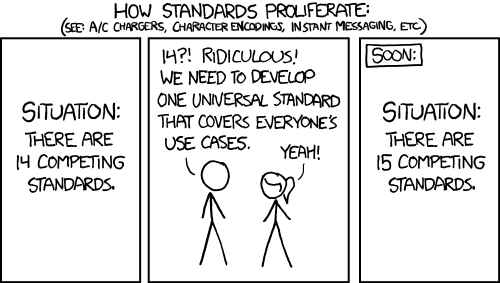

I’m sure it’s fun to imagine that comic strip has an answer for everything but it doesn’t. Sometimes it doesn’t apply, as perhaps in this case. How many so-called standards are there for the process by which someone in the United States is paid by check? I believe there’s only one and, perhaps not coincidentally, it’s managed by the Federal Reserve, the same body promoting this new system. For that reason, it seems more likely it will become the universal payment service.

I believe that it is an implementation of “ISO 20022: Financial services – Universal financial industry message scheme”. It’s intended to be interoperable internationally.

ISO 20022 is a replacement for the cheque processing process, in the sense that it replaces cheques.

In Aus, the actual “cheque processing process” has already been entirely replaced by a digital / electronic system anyway: paper cheques are not used in the clearing system here, they are destroyed early in the process. I don’t know how far the USA has gone in that direction.

US practice since ~2005 has been that the financial institution first accepting the deposited check scans and destroys it. Everything downstream runs electronically off the scan.

Right. My understanding of the history here is that until about 25 years ago, when you deposited a check (perhaps one from a far distant bank) at your local bank, it was then flown across the United States to be processed at the originating bank. And then one day in September 2001, some people flew planes into buildings, killing thousands. As part of the response, the airspace was closed in the entire country for about a week. Processing of checks was held up. That prompted the development of a new process involving scanning of checks (and allows you to deposit a check using a smartphone app). (Forgive me if I’ve muddled some of the details.)

But America still has paper checks, unlike some (many?) other countries. That’s what something like the FedNow Service might be able to replace entirely.