I imagine the sales push consists of pretty words and a slick brochure or two. Next time you see this guy, tell him that you are interested but you want to see the actual contract, which is probably 20 or more pages. Sit down with him and have him explain Every. Single. Paragraph. to you in detail and to your satisfaction. I suspect he won’t be too excited about that, and afterwards you probably won’t be either.

That’s what they prey on. And I think the phrase ‘trustworthy annuity vendor’ is as close to an example of an oxymoron as you can find.

Take Buffet’s advice: if you aren’t willing to spend quite a lot of time on managing your investments, just put the money in a low-cost index fund.

I don’t have any reason to doubt that Fidelity’s annuities do anything other than what they say on the tin:

It looks like their expected profit is 0.25% per year. Realistically, that just gives them an incentive to see that it does well.

Buffett was talking about the wisest choice. That’s different from the most realistic choice.

My wife was looking for an annuity to put 1/3 of her retirement funds into (about 6% of our net worth, so I wasn’t going to fight it).

My brother is a financial planner/advisor. A very bad one from a clients point of view. He told her to use Fidelity as he would never ever recommend that to his clients.

He’s a fiduciary!

That’s apparently on top of their fund fees. And they have no incentive to use their lowest cost funds …

Their own take from their FAQs:

We believe that when saving for retirement you should first contribute as much as you can to your employer-sponsored plan and IRA. Maximizing an employer-sponsored plan and IRA first allows you to take full advantage of any available company match, pretax contributions, and tax deductibility. Once you’ve reached those thresholds and would like additional retirement savings opportunities, you may want to consider contributing to a low-cost, tax-deferred variable annuity so you can add to your tax-deferred savings.

If I am understanding correctly the sales pitch is that someone currently in a high tax bracket who has maxed out on other tax deferred vehicles may consider paying the extra fee on top as worth it to put more tax deferred. Like why tax free bonds are attractive at lower returns for high earners?

Sorry to nitpick, but I don’t quite understand the distinction?

Let’s say that Robert’s 4 year old daughter was kidnapped and is being ransomed back to him.

For each person that pays a kidnapper for the return of their child, there’s greater incentive for bad guys to target and kidnap more children. Likewise, knowing that Robert is someone who will pay out, the ransomers have little incentive to give the kid to him, until they’re confident that he’s been bled dry - they’re likely to just string him along for as long as possible. At that point, their best play is to kill the kid, because they’re at the greatest risk of getting captured by the police when trying to perform a swap.

The wisest answer is for Robert to forego his child and wish the kidnappers a good life with their new liability. The realistic answer is to tell Robert to get proof of life and proof of health. There’s just no real world where he takes option 1.

Forgive me, but you seem to be going off on a rather wild tangent not clearly related to investment?

But I will agree to drop it. I don’t want to start a hijack flamewar.

I am still not a fan of annuities.

Sorry, I didn’t realize the annuity being referred to was a variable annuity. My wife bought a fixed annuity. Basically insurance against “outliving your assets” but at a cost and the risk that inflation may render the fixed payment

She’s terrified of an asset bubble bursting and her life savings being vaporized. I could not convince her that if all the companies in the world are worthless, states and municipalities default on their bonds and even the US treasury defaults, the insurance company backing her annuity isn’t going to be solvent either.

I’m not sure if the addresses the wisest vs most realistic choice.

As Keynes said: in the long run, we are all dead. In a collapse like that, probably only a few hunter-gatherer communities might survive… assuming their environment hasn’t been destroyed by strip mining or deforestation etc….

We are all (at least in the US and Europe) totally dependent on a massive global infrastructure that has been built up over many decades. As has been discussed several times upthread: is this stable long term?

I don’t think we know. Maybe one critical failure could bring down it down like a house of cards? Or does it have enough negative feedback corrections to keep it running? Only time will tell…

My mother (late 70s) recently bought into an annuity of some type offered by TIAA. I’m sure it’s not a scam, but I don’t think it is the wisest financial move. She is extremely risk adverse when it comes to money, so really likes the idea she is guaranteed a payment of a fixed amount every month.

When I looked at all of the numbers it probably would have been better to keep the money in almost any type of equity, and just pull it out as needed, but

is her main concern.

I think this annuity guarantees a minimum monthly payout until death, but it can also go up or down from the expected monthly payout depending on investment performance. If she dies before the annuity expires, I’ll inherit some of the principle, and the annuity was probably a financial loss. If she lives past the expiration of the annuity, she’ll continue to collect monthly payouts, and then it was probably a financial win for her.

My take is that it’s a way for TIAA to bet on their clients’ deaths.

My Fidelity rep recommended a fixed annuity with approx 5% of my assets. It pays 4.8% over 5 years, and I can withdraw up to 10%/year without a penalty.

I always had a fairly jaundiced view of annuities and equated them with scams. But I wanted to diversify my portfolio and this looked pretty solid to me:

What am I missing, though? The Fidelity Total Bond Index (FTBFX) pays 4.8% and I can withdraw 100% at any time without penalty.

I know FTBFX yield can go down, but it can also go up.

Absolutely true! But I already have about 50% of my assets in assorted Fidelity low- or zero-fee bond index funds – this was suggested mainly as a diversification strategy.

That you can withdraw is the downside. Most people will end up blowing their savings at some point. The advantage of an annuity is that it wholly removes the weakest link from the chain.

If that’s not you, then they’re a waste of time.

Former advisor here with a fair bit of experience with annuities of many flavors. I will admit that the term “back loaded annuity” had me scratching my head, but after some sleuthing, it sounds like we’re dealing with a variable indexed annuity (VIA).

I hate annuities. I think they are, mostly, overly complicated investment vehicles that are overly complicated by design to keep you confused and hand off decision-making to your advisor. If someone held a gun to my head and told me to invest 50% of my assets in an annuity, I’d probably go with a VIA.

There are no fees in a VIA, other than opportunity cost. The mechanism is something like this: you give Annuity Company $100,000 and put it in a VIA. For the duration of its time in there, the funds are tied to an index (let’s say the S&P 500 - but usually you have an assortment of options). You then get to participate in the growth of the SP500, up to a certain percentage. This varies by annuity company and by index. Let’s say this one is capped at 60% for 6 years.

What does that mean? It means that after 6 years, if the S&P 500 has increased by 60%, your account is worth $160,000. If it has increased by 320%, your account is worth $160,000. If it has increased 4%, your account is worth $104,000.

What if the S&P 500 has decreased over that time? Well, this is where a VIA may be really attractive to some people. In this case, your account would be worth $100,000. Complete downside protection, zero fees.

The catch is two-fold - if the index increases by more than the cap, the annuity company keeps the difference. The other is that if you take your money out before the 6-year surrender period, they assess significant penalties.

As such, this is a TERRIBLE product for someone in their 90s. Pullin, I suggest reporting that advisor to his firm for elder abuse. There is a hotline to do so: 833-372-8311.

Sounds like a multi-year guaranteed annuity (MYGA). Both these and single payment immediate annuities (SPIA) are the way to go if you are going to put funds in an annuity. Straightforward, low cost, and fairly simple. Not nearly as lucrative for insurance agents as more complex types such as indexed annuities. General consensus at forums like bogleheads and early retirement is that MYGAs are a solid choice if they meet your needs.

Backing out to broader discussion -

I’ve previously on these boards bemoaned that “risk” is used by investment companies and academics as a synonym for “volatility” … in that regard an article summarized here is of interest:

The authors begin by challenging the foundational assumptions behind traditional risk-based models like the Capital Asset Pricing Model (CAPM) and the Efficient Market Hypothesis. They present a historical and empirical autopsy of the idea that taking on more risk necessarily leads to higher returns. Their analysis shows periods—some lasting decades—where equities failed to outperform supposedly “safer” government bonds, both in the U.S. and internationally. Far from being anomalies, these episodes are seen as repeated failures of risk theory to explain actual investor outcomes. Instead, Arnott and McQuarrie argue that human emotions—especially fear of loss (FoLI) and fear of missing out (FoMO)—offer a more compelling explanation for investor behavior and asset price movement over time.

Part of the point is that it isn’t greed that drives market irrationality, but fear, and which fear is bigger at any particular time, fear of loss, or fear of missing out. And that while that results in irrational (“deranged”) pricing in the market (see TSLA) the fears are very rational and easy to understand from the fund manager to individual investor viewpoints.

Well done!

I’ve long said that the market and hence asset prices, is fundamentally a social phenomenon overlaid on the top of fuzzy accounting.

Now throw meme stocks, social media manipulation, and AI into the mix and the market can not only remain irrational longer than you can remain solvent, it can remain irrational indefinitely.

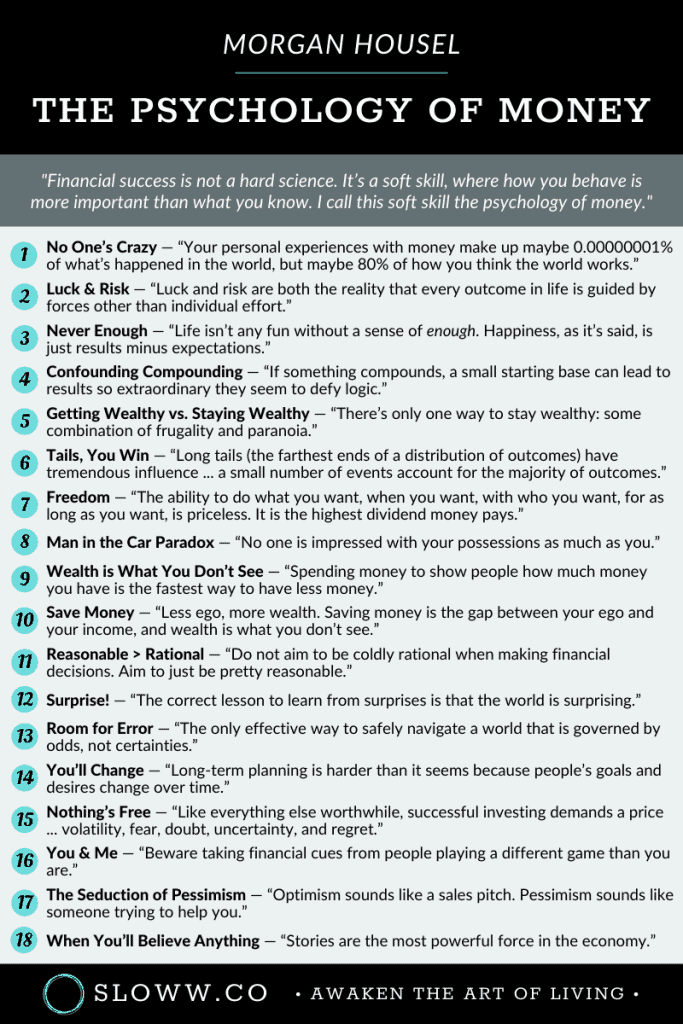

I have read the book “The Psychology of Money” by Morgan Housel several times. One of my favorites and well worth the read (or listen) for anyone. Also a very easy read.

If you don’t want to read it, to give you a sense of it, here are one-sentence overviews of the Chapters: