Looking ahead 30 years is far too difficult. But I think there’s a fair chance that ten years, or perhaps even five years, from now some of the comments in this thread will appear short-sighted. Gold and silver (and copper) have been widely used as money for over 3000 years. China is famous for its paper money 900 years ago, but that paper was itself a promise by China’s government to redeem for metal. As late as the 1960’s the world price for gold was still the $35 rate set by the U.S. Congress. Yes, central bank “fiat” money has been successful for almost 50 years. But past performance is no guarantee of future results.

Nobody knows how the world’s currencies will evolve. There is a key difference between economics and other sciences. Nobody needs to drop balls from atop the Tower of Pisa anymore — (yes I know even Galileo probably never did this!) — been there; done that; know the answer. But the human constructs that economists seek to understand are constantly evolving.

For example, interest rates were once a useful indicator, informing us about the supply of and demand for ready cash. Now interest rates are effectively fixed by central banks. Are the unusually low interest rates we see today — what one financial analyst calls “the bubble in ‘risk-free’ assets” — cause for fear? Maybe, maybe not. One frequently hears analysts add “MMT” to their vocabulary today; I’m not sure if they’re celebrating a wonderful new paradigm, or being sarcastic!

The U.S. remains the world’s strong prestige currency. Other major economies suffer the same possible perils as the U.S.: high debt, low interest rates. When people wonder about a possible “currency collapse” I do NOT think they’re talking about USD-$ plunging against EUR-€ and GBP-£. The worry is about a global collapse, perhaps with a cycle of devaluations or general inflation. (BTW, Japan is often cited as proof that high debt and low interest are not problems. But the Japanese economy has special strengths that many of the Western economies lack.)

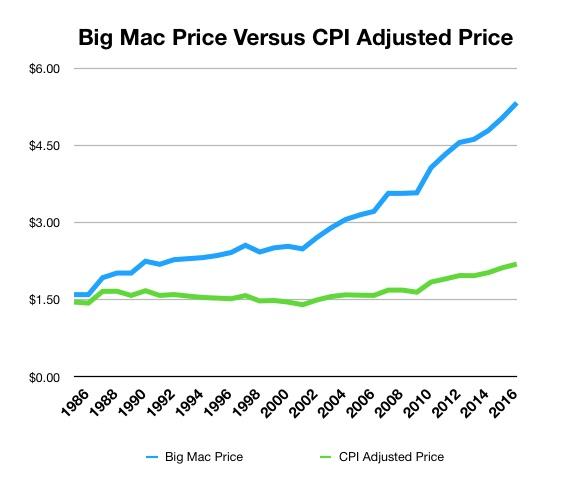

I think OP is wrong to worry about the dollar “constantly being devalued.” Inflation is about 2%, just where many policy makers want it. (Some would like the flexibility offered by slightly higher inflation.) In normal times, you’d make up for the lost value of cash with interest on your cash savings. (Gold and silver don’t pay interest.)

Of course in these abnormal times, savings accounts do not pay enough interest to beat inflation. So you get a higher return by buying stocks or junk bonds. Maybe. Do the low interest rates tell a supply/demand story? The world is awash in money, while demand is low (even Berkshire-Hathaway can’t find anything better to do with its cash than buy back its own stock).

A bigger problem with the low interest rates is that central banks have lost their main tool for combating recession. From 1989 to 1993 the Fedfunds rate was lowered from 10% to 3% to combat recession. In the early 2000s the rate was lowered from 6.5% to 1%. From summer of 2007 to the end of 2008, the rate was dropped from over 5% to about 0%. See similar responses in other recessions. The Fedfunds rate is only 2% now: there’s not enough room to drop it. (Deliberate inflation may be the simplest way to lower real interest rates!) Deficit spending is the other way governments fight recession. But we now have a trillion-dollar deficit in good times! For the next recession … up the deficit to TWO-trillion dollars?

And cryptocurrencies — increasingly seen as a way to evade taxes and regulations — might reduce demand for central banks’ money.

NO, I think some of the confidence shown in this thread is overly sanguine. Most individual investors are already diversified into hard assets (including real estate) by virtue of home ownership, but renters should put some of their savings into a “hedge” asset. Central banks themselves understand this: “After a relatively modest net increase of 13.9 tons in July, central banks globally took in a net 57.3 tons of gold in August.”

{kind=link}

{kind=link}