The point of securitizing debt is to remove risk from your balance sheet by selling the debt.

Essentially, you’re just transferring the risk onto another party, right? Which is fine… unless you yourself start buying securitized debt, meaning that you are taking on risk yourself. Which is what all the banks/investment firms did. Therefore, no risk was transferred at all.

THEN you had the quants. “Quants” are mathematicians hired by the firms to slice and dice this debt even more, create derivatives out of it, etc. By 2007, the deals were so complex, nobody really knew who owned what. So when Lehman collapsed, nobody knew how much their assets were worth because nobody really knew how exposed they were to Lehman Brothers.

Here’s a link to a complex CDO deal.

{kind=link}

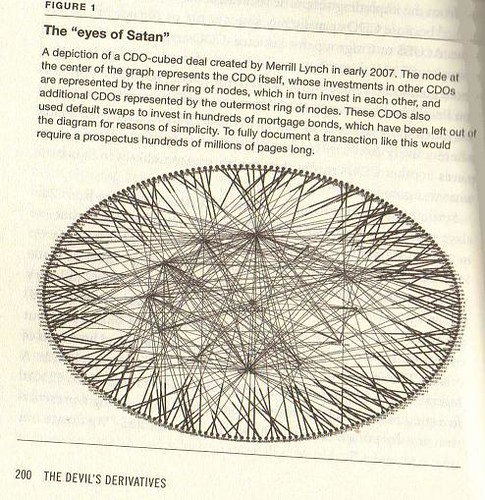

The above image is taken from page 200 of Nicholas Dunbar’s The Devil’s Derivatives, in my opinion one of the finest layman books written about the 2008 crisis. (Sorry for the sucky scan, but it came out clean enough imho.) Each of the dots around the edge (and the dots scattered around the middle) represent other CDO’s which made up this particular derivative (This derivative is represented by the dot in the middle of the Eye.)

Not shown in this picture are the hundreds of mortgage bonds (which, in turn, represent the tens-of-thousands of mortgages that make up the assets of the bonds), from which the value of the derivatives are derived. Remember: each of the outside dots represented hundreds of mortgages.

While there were problems in the market prior to September 8th, the official collapse of Lehman Brothers (LB) on that date meant that some of these “dots” were now worthless, the assets behind them either tied up in bankruptcy court, or seized by other counterparties.

Trying to figure out which of the outside dots were LB-backed CDO’s (or which of those dots had LB mortgage bonds within them), was a horrendously difficult task just for this one CDO-cubed derivative. Multiply that by every derivative in the world which may or may not have had LB-backed assets, and it’s no wonder that the markets froze - as I said, nobody knew what their exposure was to LB, which meant that nobody had any idea what the value/price of the CDO should be.

Ergo, panic.