What I find interesting is that we’re using some of the same primary sources of information to argue competing viewpoints. The IEA must be used to this.

Well, part of that is that the IEA’s own position has shifted over the years, from a (lowercase) peak oil stance, to statements about the US and Canada being net oil producers (and an upward revision of when peak oil will occur to several more decades in the future) to their current, more circumspect assessments. Part of it is interpretations of what’s being said. ralfy obviously is interpreting things and looking at snapshots in time from places like the IEA that bolster his view on what’s happening…and others in this thread are doing the same thing but, but seeing a different picture.

I found this article that you and others might find interesting that sort of goes into this, especially from the IEA’s stance.

Anyway, you can read the whole article. It goes into a lot of other aspects of this debate that concern global climate change, which isn’t really addressed much in the usual peak oil/Peak Oil™ threads, but one that will also have an impact on our actual use of fossil fuels…after all, even if we HAVE the resources available, we might not end up using them (and thus, oil will certain peak and decline due to natural market forces) anyway, and with new alternatives being looked into, that’s my own bet on the trajectory. We’ll keep using the stuff for the near future, the price will continue to rise, and eventually new technologies will become viable as a certain price point in oil/fossil fuels is reached making a transition possible and natural for the market. ralfy obviously feels differently, and even though s/he hasn’t come out and said it, has a more gloomy outlook on the future.

Interesting side note:

Not sure what this says about the long-term viability of high-tech exploration or how it will affect production through the peak era.

Pretty much on par with people who talk about Global Warming and then protest when someone wants to put a wind farm in their scenic location.

According to the articles that I shared earlier, more wells have to be drilled each time just to maintain production rate. That means extraction has not been more efficient but the opposite.

And except for coal they have even lower energy returns compared to shale oil, especially biofuels.

From what I know, it has been known for several decades:

and employed because we need to use unconventional production. And we need that because energy return for conventional production has dropped.

In short, we now have lower energy returns for many forms of oil and gas but high energy return needs.

That’s all part of peak oil.

The problem isn’t reserves but production. As I explained earlier, we actually have hundreds of years’ worth of crude oil, but crude oil production flattened out anyway, and we’re now resorting to unconventional production.

Again, that’s peak oil:

“The only true metric of energy abundance: The rate of flow”

According to the EIA, the IEA, and others, it will reach only a few Mb/d before peaking in a few years. That’s nowhere close to Saudi Arabia production which lasted several decades.

See the Slate article shared earlier for details.

Unfortunately, efficiency in a global capitalist economy leads to more consumption, not less.

Also, I’d like to look at charts for “renewable generation per capita”.

Meanwhile, try the chart in the EROI article I shared many times in previous articles. That chart says quite a lot.

[quote]

I don’t think that is true anymore. If recoverable shale reserves exceed 1.5 trillion barrels, and they weren’t recoverable at all until the last 7 years or so, I’d say we are currently in the era of the largest discoveries in history.

[quote]

Any charts showing updated discoveries are welcome. Perhaps you can share that and the one for renewable generation in your next post.

Please take a look at the charts shared here:

Also, note the other articles shared earlier where the IEA argues why other countries will not be able to replicate what the U.S. did.

Third, consider the point raised by the IEA about shale oil not lasting (a point confirmed even in other reports).

Finally, note expected increase in demand as almost half of the world’s population will require more oil and other resources to maintain middle class conveniences. See the BBC and Guardian articles shared earlier for details.

The second article states that in order to meet a decline in crude oil production, more significant increase in oil demand per year, and low energy returns for shale oil, we will need the equivalent of one Saudi Arabia in new oil every three to four years, far higher than the norm, which is one every seven years, as discussed in the IEA report shared earlier.

Unfortunately, the price is not set by producers but by the market. Thus, producers face rising costs while the market cannot handle higher prices.

Meanwhile,

“Shale Drillers Feast on Junk Debt to Stay on Treadmill”

I think different data sets are used for the viewpoints. On one side are reserves. On the other, production rate.

Peak oil is about the latter.

From what I know, the IEA view shifted because they did a comprehensive study of the matter. As I recall, in 2006 they argued that crude oil production will peak only after many years. In 2008, they conducted a detailed study of hundreds of oil fields. In 2010, they released a report acknowledging that crude oil production peaked in 2006. This was finally confirmed in EIA data presented in my first post in this thread.

Finally, FWIW, I am not the only one who has such an assessment of the future. Several military forces, intelligence organizations, businesses, regulatory agencies, and other groups have similar views. The reports are shared here:

https://sites.google.com/site/peakoilreports/

Again, I do not intend to flood the thread with links. Rather, I want to point out that this issue is being taken very seriously by various authorities.

To find out about one of them, consider the points from the IEA report which I shared several times in previous messages.

Ok, we’re talking about the same thing from different angles. The Hubbert peak oil theory says that EROI will decline as discoveries wane and wells get depleted. It is pretty much just common sense- old wells have lost their pressure and therefore it is going to cost more money to get that oil out.

But horizontal drilling through shale changes the equation. Suddenly whole new reserves become available, reversing the ‘declining discoveries’ aspect of peak oil. Also, if I’m not mistaken, horizontal drilling through shale introduced an increase in EROI over some other forms of drilling. It isn’t a great figure and not as good as we used to get, but OTOH it is still kind of a new technology and the EROI for it is actually increasing (though it still isn’t that great on those terms).

So, there are vast new reserves of more expensive oil, but it is getting incrementally less expensive to extract it.

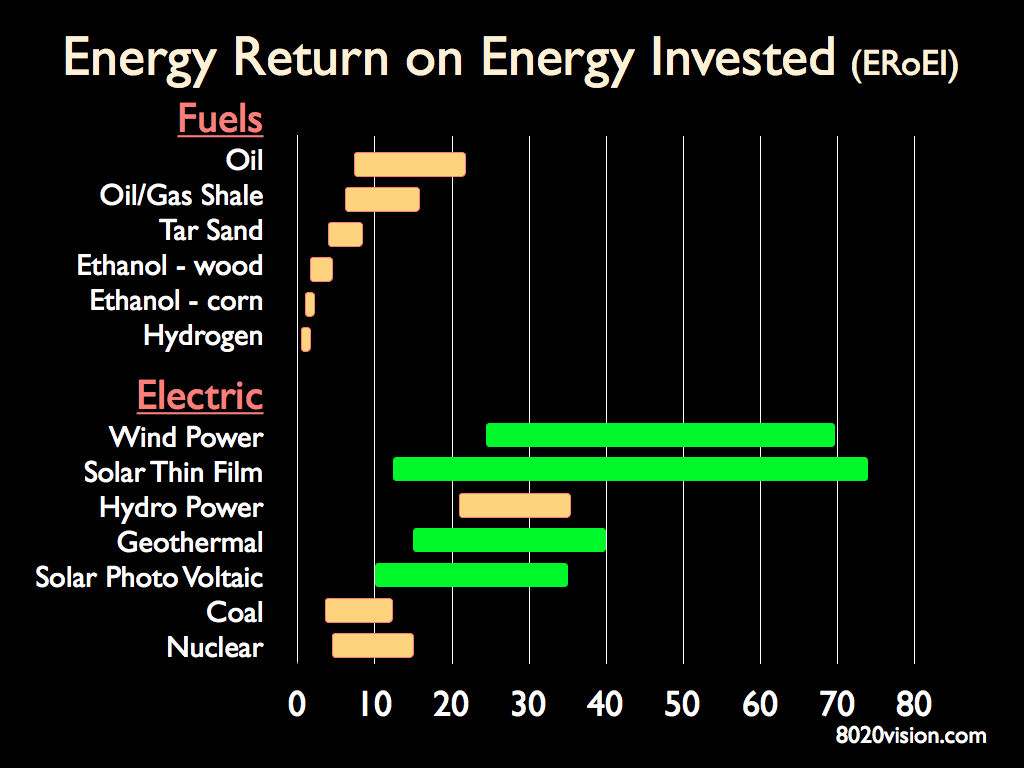

Here’s an EROI chart for various fuels. Wind and solar look just fine. If you don’t like these numbers, I’ll point out that the chart you referenced was from 2008 and these are rapidly changing fields.

{kind=link}

Alright, I figured out our difference here- horizontal drilling is a subset of directional drilling. Horizontal drilling into shale has only been around AFAIK for 7 or 8 years.

I agree. The EROI for horizontal drilling doesn’t look so great from what I read. But from what I gather that EROI is increasing.

Well, yes and no. Yes, crude oil production is following Hubbert’s model. I expect shale oil will too. But shale oil represents a kind of ‘reset button’. These are vast new resources that are only now being tapped. Instead of EROI going on a steady decline down to 1, it looks like it plateaus or even increases a little for shale oil, even though I still agree with you that the EROI of shale oil isn’t that great.

There are conflicting reports about this. It isn’t clear what to believe.

I dunno. If someone drives to and from work, and one day buys a plug-in hybrid that gets 100mpg, is he going to drive so many miles that he ends up burning more gas than before? Not necessarily.

You’ll have to divide by the population of Earth, but here is an article about global renewable generation:

It is actually pretty impressive.

Speaking of solar growing fast, I think it is about to speed up quite a lot. Look at this chart. 7% of global electricity from PV by 2020, and it’ll be cheaper than coal power! I think we’re going to see a lot of PV.

{kind=link}

This is just a wiki about shale reserves. On the one hand, shale reserves in this source appear to be trillions of barrels more than I’ve been claiming. OTOH, other sources claim China has the world’s largest shale reserves, so maybe this isn’t quite accurate, but it is a start.

How many terawatts is one Saudi Arabia?

Ralfy, I also wanted to share this article with you. It is kind of a mixed bag- it points out that the oil majors are getting ‘eaten alive’ in their exploration costs, are cutting back on exploration in response, which is going to cause problems down the road. OTOH it claims that 3 million barrels a day of production are off the market right now because of various kinds of turmoil, and that there is an oil glut coming, which will cause a crash and then a spike in prices. There is some peak-oily stuff in there, but some of it seems to also contradict (immanent) peak oil.

This is the reason why crude oil production peaked. It is now down to something like a 20:1 return.

The problem with shale oil is that decline curves are steep, i.e., each well does not last very long. That means more wells have to be drilled each time to maintain production. That will ultimately lead to high capital expenditures which have to be passed on to buyers. But oil producers don’t set the oil prices. That means we face a market that can barely tolerate high prices and producers who are forced to raise prices to cover their costs.

On top of that, the IEA argues that what the U.S. did cannot be replicated elsewhere. The implication is that U.S. shale oil is the only thing keeping the global economy afloat, it will last for only a few years, and it will have to cover both increasing oil demand plus a drop in crude oil production.

From what I gathered, there are vast reserves for much of oil and gas. The problem is that it is becoming more expensive to get them, which is why oil price is triple what it should be, and why shale oil will last only for a few years. More details are given in the Slate article shared earlier.

I cannot find the sources of the figures given in the chart.

The point to consider is that the source of what is drilled does not allow for high energy returns. In all cases, more wells have to be drilled each time to maintain production. The cause of that are physical factors directly related to peak oil.

My understanding is that the EROI for unconventional production is low and will remain so, likely because production decline take place faster.

I cannot find any source that shows it to be a reset button. Even the most optimistic view shows that shale oil production will peak in 2020, showing a production cycle far shorter than crude oil.

Please mention the identity of those conflicting reports.

The gas that is not used will be sold to someone else. Businesses do not stockpile oil at a loss but will sell to the highest bidder. And given increasing demand not only for oil but even for the material resources to make hybrids (and the oil and mineral resources to make hybrids are significant), not to mention over a quadrillion dollars (notional value) in unregulated derivatives riding on a global economy a fraction of that, I highly doubt that conservation will take place.

Why not look at energy and material resources in general against population, such as ecological footprint? That’s based on the assumption that the global economy does not run only on electricity. Thus,

For the 2006 global population, we have a bio-capacity that will only be enough to sustain living standards equivalent to that of Cuba (likely, no expensive hybrids), but ave. global footprint had already exceeded bio-capacity, which means we have been in overshoot for some time. Worse, that population will continue to increase while bio-capacity will drop due to a combination of environmental destruction and global warming.

Can the global economy, which requires continuous economic growth based on increasing production and consumption of resources, be sustained given that?

That’s a certainty, but I don’t think most energy sources used together will meet the needs of a growing global economy. At the very least, it might be able to meet basic needs, but that will require extensive cooperation between economies, something that has not taken place for decades. I explained that more than once in previous messages.

The problem is not reserves but production rate. According to the IEA and others, production will peak in only a few years.

I don’t know, but the point is based on oil demand per capita the last few decades needed to maintain economic growth. According to the IEA, an oil demand increase of up to 2 pct per annum needed to sustain such growth is equivalent to one Saudi Arabia every seven years. More details are found in the IEA 2010 report shared earlier.

But to meet a growing global middle class (see the BBC article shared earlier), we will need the equivalent of one Saudi Arabia every 3-4 years (see the Guardian article shared earlier).

The reason for this is that significant components of manufacturing and food production do not run on electricity but require fossil fuels for heavy machinery, cargo ships, and petrochemicals.

Theoretically, it is possible to use electricity for all of these, but that will require a transition period that will span decades. More details are given in the study presented in the Business Insider article shared earlier.

In many ways, 3 Mb/d is small if global oil demand has to rise by up to 2 pct a year, or around 1-2 Mb/d. Related details are given here:

“How much oil growth do we need to support world GDP growth?”

Also, we might be looking at a glut caused by economic crisis, after which recovery leads to increasing demand, then another price spike because supply can’t meet demand, then economic crisis again. Thus, we face what is essentially the first part of peak oil, i.e., oil production peaking or unable to meet demand:

“Our Oil-Constrained Future”

I am going to second what XT said and ask you to follow our example in the use of cites. That is, when referring to a cite, please state what your point is, post a link to the cite, and also post the relevant quote from that cite in your message. It is just so much more clear and useful that way.

I’d especially like you to follow this advice at least on this one point. I’ve just shown you a cite that claims shale oil reserves in the US alone exceed 4.5 trillion barrels. These reserves have only begun to be tapped in the last decade (compared to conventional oil which was first tapped in the 1860s, but only in earnest I guess about 100 years ago). It is more expensive and difficult to extract- I’m not debating that point so we might as well quit returning to that. But why such large, freshly tapped reserves are doomed to peter out in just a few years is a mystery to me. Lots of wells need to be drilled? I get it! But these deposits span thousands of square miles (the Bakken IIRC contains 25,000 square miles of drillable oil shale). That can support an awful lot of wells.

So, on this point, if you don’t mind, would you please post a link to the relevant cite, state what your point is, and cut and paste the relevant quote(s) from it in your reply? I think that would be a lot more clear for everyone.

Given the choice between going down the drain and doing something to address the problem, it seems inconsistent to just write off the solution to the problem as ‘too hard’ and go back to singing the dirge of doom. I don’t think oil supply can (or should) increase very significantly from where it is today. But I also think we can deal with it- it isn’t really oil (exclusively) the world needs, but energy. Other energy sources are becoming or already are more efficient than what we use today. I don’t see any point in letting crying about the end of the oil era stop us from addressing our problems.

I’ll have to get back to the rest later.

I cited the source several times in previous messages. See the CSM article.

For an overall view, see the IEA 2010 report (cited and referred to multiple times).

Peak oil is not about reserves but about production rate. That’s why even with trillions of barrels in reserves, shale oil production will still peak by 2020.

In fact, the same phenomenon can be seen with crude oil. We have trillions of barrels of that underground, and yet crude oil production still peaked in 2005.

I explained both points very clearly many times in previous messages and using several sources.

Multiple sources were provided in previous messages, from the IEA 2010 report to various articles from Bloomberg, CMS, Guardian, and others, to Kopits’ lecture, features from ABC, and more.

All of the points were also stated very clearly at least more than once. However, I will be happy to state them again, but you need to go to my previous messages to see the references. (By the way, in contrast to what I’ve been sharing, I am disappointed by the quality of references or lack of it given to counter my arguments.)

According to the EIA, crude oil production peaked in 2005. U.S. shale oil production is now meeting increasing demand.

According to the IEA, U.S. shale production will last for only a few years. The reasons given by geologists featured in the Slate article are: decline curves are steep, and more wells have to be drilled each time just to maintain production. This explains why energy return for shale oil is not high.

As pointed out in the Kopits lecture, this explains why capital expenditures are soaring. This, in turn, explains why, according to one Oil Drum article, crude oil production for five major players have dropped by a quarter since 2005.

What to expect? According to the IEA 2010 report, we will at best see total oil and gas production globally increase by only 9 pct. However, that is based on the assumption that crude oil production will flatten out indefinitely. See the chart presented in the report as well as in various media for details. See the first chart presented in this article for details:

Do you see the blue, grey, and light blue regions, i.e., the three lower regions in the chart? It shows crude oil production flattening out, thus allowing world oil production to keep rising thanks to natural gas liquids and unconventional production.

What’s the catch? According to Aleklett and others featured in the ABC feature on crude oil, that plateau can only be possible if historical flow rates are not considered. In addition, given rising expenditures, crude oil producers will continue producing with diminishing returns. See the Kopits lecture for details.

In addition, even a 9-pct increase in total oil and gas production, will not be enough to meet an oil demand that has been going up by 1-2 pct each year (explained in the IEA report and the ABC feature; this is equivalent, according to the IEA, of one Saudi Arabia of new oil production put online every seven years). That’s why the same IEA report argues that at least 70 pct of oil demand increase each year has to be replaced by renewable energy, and that strong government policies plus cooperation between economies has to take place.

What’s the problem with these? We live in a global capitalist system which goes against cooperation. It requires increasing production and consumption of energy and material resources coupled with increasing credit. That’s why, according to the BBC article (again, cited earlier and referred to many times), we expect a growing global middle class during the same years.

In order for that middle class to grow, oil demand (and material resource demand) has to grow even faster. To meet that plus an expected drop in crude oil production (see the trend line for spare capacity from a Morgan Stanley chart presented by Business Insider and cited earlier), unconventional production has to rise even faster. How much more? According to the Guardian article, we need one Saudi Arabia every three or four years, or double what the IEA argued.

Thus, how does unconventional production, which according to several articles shared earlier (from Globe and Mail, CSM, Slate and others) provide that when it is expected to peak in only a few years, and when according to the IEA (see the same CSM article) U.S. shale oil production cannot be replicated elsewhere?

Even the most optimistic view (see the IEA report mentioned repeatedly) shows total oil production going up by only 9 pct during the next two decades, and that’s assuming that crude oil production will flatten out.

Also, FWIW, the IEA does address the problem in the same report, arguing that in order to maintain economic growth, we will have to replace at least 70 pct of oil demand increase per annum with renewable energy.

The problem is that the other indicators mentioned earlier put to question the points that crude oil production will flatten out, U.S. shale oil will be sustained for more than a decade, and that oil demand rate will not rise faster (i.e., there’s no growing global middle class, or no increasing demand for oil and other material resources from BRIC and emerging markets).

One more point: all energy sources have low quality and quantity compared to what countries like the U.S. need (see the EROI article shared and referred to multiple times).

One more point: one is free to look at this issue in terms of overall material resources. One example is ecological footprint, which was mentioned and cited in my previous post.

What that reveals is that our ave. footprint per capita as of 2006 is 2.7 global hectares (equivalent to the average of Turkey). The biocapacity of the earth is only 1.8 (equivalent to the average of Cuba).

That ave. footprint is expected to increase as the global middle class grows (e.g., more cars, construction materials, electronic gadgets, resource-hungry food, etc., purchased) while biocapacity drops due to a combination of increasing global population plus environmental damage coupled with global warming.

For the latter point, there are many sources to consider, including an expected global water crisis, fish harvest declines, arable land damaged due to global warming, etc.

The reason why this should be noted is that the same IEA report sees peak oil combined with global warming as two critical problems that we will have to deal with in the long term.

The report (shared and cited many times):

https://www.iea.org/publications/freepublications/publication/name,27324,en.html

and an article where the IEA warns of this related problem:

“World headed for irreversible climate change in five years, IEA warns”

The problem is that the unconventional fossil fuels that we will need to use to make up for a lack of crude oil may add to greenhouse gas emissions.

Well, it is always true that there is no set of decisions we can choose such that nothing bad at all will happen. Still…

Really? Your answer is “no”? I suggested this pages ago, and others have also requested that you quote the passage relevant to your point next to the links to your cites. I’m not claiming your argument falls if you won’t do this, but if you are only willing to repeat the same things over and over again, in the face of multiple promptings, I’m afraid I may not be able to prevent XT or maybe some ancient 'doper from administering a Turing test. Meanwhile, someday I may manage to dig through this whole thread to find the cites you’re referring to, and then examine those cites in detail until I find the parts that I think are the support for your points. Then, I’ll weigh it all and come to some sort of preliminary conclusion- I’ll have to run it past the board first, of course. I’m soooo busy already- if only there were a faster way! ![]()

Anyway, to a previous point

I suppose my view is more optimistic than those you are acquainted with. I’m referring to the Hubbert Peak Oil theory. First, look at this. Things are not actually proceeding according to Hubbert’s predictions, no?

{kind=link}

I think Hubbert’s theory is broadly true- oil production necessarily will peak someday. But the assumptions on which he based his theory decades ago have been replaced with new assumptions.

We still have ~1.5 trillion bbl of recoverable crude, and that resource does appear to be peaking. The unexpected thing is that shale oil reserves are significantly larger than anyone was predicting. Trillions of barrels in discoveries, of essentially virgin, untouched resources (in stark contrast to Hubbert’s assumption of declining discoveries), just entering from the left onto the Hubbert Curve. That’s why it is a ‘reset’ button. Shale oil reserves are larger than crude oil reserves, a new discovery, and therefore are themselves at the beginning of the Hubbert curve, even if crude reserves are not.

Also consider the unconventional geology of shale oil deposits. They can be as flat and uniform as the plains themselves. You get an ‘oreo cookie’ effect that goes on for miles in every direction- 100m (?) or so of shale oil sandwiched in between layers of shale rock. There are sweet spots that the good wildcatters are exploiting for really good profits, but in the long run it is going to be a huge, steady source of expensive oil. It isn’t a bunch of deposits of varying size and difficulty scattered around. In the long run it is all pretty much the same, so we can expect its production chart to be a lot flatter than a classic Hubbert curve.

That’s not our only problem. You will find more details in the IEA 2010 report, which I discussed more than once.

Again, I explained my arguments and referred to relevant points pages ago. See for yourself.

I am referring to crude oil production. Read the points I gave in my first post in this thread:

http://boards.straightdope.com/sdmb/showpost.php?p=17297119&postcount=78

What you want is rate of flow, not reserves. My reasons are given here:

http://boards.straightdope.com/sdmb/showpost.php?p=17300166&postcount=99

Keep in mind that they go for the sweet spots first, which explains why depletion rates are steep and why shale oil will last for only a few years. The reasons are given in the Businesweek article linked here:

http://boards.straightdope.com/sdmb/showpost.php?p=17297119&postcount=78

According to the article, 6,000 new wells have to be drilled each year just to maintain production. That’s why shale oil is expected to peak in three years or so.

But that’s not the only problem. The IEA argues that shale oil production in the U.S. cannot easily be replicated elsewhere, and demand is rising considerably. More details can be found in my previous messages, such as:

http://boards.straightdope.com/sdmb/showpost.php?p=17305650&postcount=153

“Why the Oil Industry is Running Into Major Trouble”

http://www.alternet.org/economy/why-oil-industry-running-major-trouble

First, I am not entirely sure what point you are making with your last point. Still, I will proceed.

From your cite:

I am still not convinced. I think ‘new oil’ is going to be more expensive and more plentiful.

I think I have provided sufficient explanation for this view in previous posts. Even if your article is correct about the Monterrey shale, I think other shale deposits are sufficiently vast to prove my point, hence ‘more plentiful’.

I think your article proceeds in a somewhat polemical way. It does state that the oil majors control ~13% of the world’s oil reserves, while state-run companies control 75%. The missing fraction we might as well call ‘the wildcatters’, and they matter in this context. The big producers like Chesapeake and Exxon may not be finding a lot of success in terms of profiting from shale, but that is because they are victims of their own scale. They buy billions worth of mineral rights, expecting to only ever use a fraction. The smaller guys are far more careful, zeroing in on the most profitable plays and exploiting them like crazy. They may not accomplish much more than move the needle of the global oil market, but they do matter and your article doesn’t really address them.

Also, there are reasons besides supply constrictions that account for drops in production in certain major oil-producing regions. A little more sensitivity and gregariousness might go a long way in these situations.

Back to ‘I am not entirely sure what your point is’… I personally think the takeaway is that the majors, especially gas guys like Chesapeake, are responding to pressure from renewables and are knocking themselves out to keep gas prices low long enough such that big consumers (say trucking companies, or foreign markets) commit big time to natural gas. Once they are locked in, you are going to see major price increases to pay off all these expenses. The trade-off for the consumer is that, as long as they keep paying, there really is a lot of energy that can be reliably extracted.

What are consumers supposed to do? Solar and wind are awesome, but they can’t replace oil and gas as quickly as many would like. Anyway, I don’t think this latest cite is hard evidence of peak oil. The end of cheap oil is certainly a milestone along that path, but ISTM that literal Peak Oil is still a ways off.

The whole article recapitulates all of the points and conclusion I made in previous messages.

Also, as I explained in previous messages, peak oil already took place. Put simply,

Crude oil production peaked in 2005.

Shale oil will last for only a few years, and if crude oil production dropped, it will pull down total oil and gas production.

Oil production for the five major players has dropped by 25 pct since 2005.

Oil prices have tripled.

As shown in recent articles, not only are estimates for shale oil overstated (as seen in Monterey) but production consists of drilling more wells each time just to maintain production. That’s why shale oil is seen as a “bubble”:

Demand increase is expected to be equivalent to the production level of one Saudi Arabia every three to seven years. U.S. shale oil won’t be able to meet that, and shale oil production in the U.S. will be difficult to replicate elsewhere. That’s why the IEA wants countries to focus on renewable energy.

Solar and wind are not even close to “awesome.” Their energy returns and quantities, together with that of other sources of energy, are very low. The global economy needs high energy returns and more energy each time to maintain economic growth. Otherwise, that economy will go into a permanent decline, and given unexpected events such as war, multiple natural disasters brought about by global warming, etc., might even collapse earlier than expected.

That’s why not only the IEA but even the IMF, the U.S. military, various banks and insurance organizations, and even science groups are warning of major crises brought about by a combination of peak oil, global warming coupled with environmental destruction, and increasing debt.

Given that, anything else I share in this thread will only reinforce what I already pointed out in the past.