And you’re wrong. You’re making silly generalizations from ideology instead of looking at how things actually work in health care. In a system of private health insurance, it is necessary and fundamental that all claims are adjudicated on a case-by-case basis, which means that the insurance company always has the option of denying or reducing a claim, and they do not hesitate to use every available legal means to do so. Indeed they have a fiduciary responsibility to their shareholders to minimize “medical losses”, which to them is what a claim payment is. In this way, the health insurer is forever an intrusive presence between the patient and his doctor.

Single-payer is completely different, and many people don’t seem to understand or fully appreciate this fundamental difference. The entire policy framework is laid out up front in the schedule of fees and procedures, and the set fees are also the instrument of cost control. Within this framework coverage is unconditional. Meanwhile the costs are predictably distributed over the entire population base, so they don’t have to worry about some quirk of the marketplace changing their risk factors. Single-payer and its functional equivalents are the only systems in which there is no clinical intrusion, and patients and their doctors are the only agents making decisions about medical treatment.

Where the hell do you live? Because when my mother-in-law broke her hip when staying with us, we had a social worker look in, but certainly none of that stuff. Now, a phone for someone without one who has limited mobility is a good thing - but I have a hard time thinking most social workers would be surprised at not getting another. Especially true for the case of two nurses. Though nursing care is covered and very helpful. We have a one story house so no elevator, but we installed grab bars in the shower for her, which we paid for. I think insurance covered the hospital bed. (Not fancy, but with rails.)

My father-in-law, who is 99 this week, spent a night on the floor of the bathroom and cracked some ribs when he fell. And now has moved into assisted living. A few of the things you laugh at could have saved a bunch of money.

Clearly your relative’s family thought that an elevator was useful - which it was - so letting her have full use of the house is not so funny either.

Swiss and German companies do pretty well also. We have critical mass here, great universities, and good funding from NSF and NIH. Maybe that has something to do with it.

Fairly possibly those offers would have been welcome and accepted by a family who were unable to have already provided them for themselves.

I’m not sure how increasing pain and deprivation incentivises a 70-yr-old with terminal cancer to go out and make enough money to alleviate that teaching discomfort.

Unless obtaining it with a sawn-off shotgun counts.

Yeah, no kidding. Medical research comes from government, universities, non-profit foundations, the pharmaceutical industry, and some private technology companies, not so much from the useless, parasitical health insurance industry – the only major industry that is quite literally worse than useless.

Government is force. Under single payer, while ignoring the possibility of supplemental payers for the sake of simplicity, I don’t have much choice to go to insurer A or insurer B. That’s intrusive. Under private payer, if I don’t like the practices of insurer A I can go to insurer B.

My relative was living in SF.

I don’t laugh at any of these things. I just don’t think it’s the proper role of government to provide people with certain things, mobile phones included. The thread asked for arguments against single payer - this is my main argument. It’s actually quite a common position. Any argument that speaks to efficiency of single payer or other systems are disconnected from the reality that a large portion of the country like me don’t think the government should not be paying for health care.

I don’t. If it weren’t for government regulations private insurance would be much more intrusive than they currently are. They’d want to know and control every minutia of your lifestyle. The public wouldn’t put up with that from the government (left and right would both push-back), but they wouldn’t have much say if insurance did it and market forces wouldn’t help since they’d all be doing it.

This is anecdotal, but I’ve had many more headaches in trying to deal with Blue Cross than my mother has in dealing with Medicare, and she is a greater consumer of healthcare than I am.

No. Are you? Let us by all means look at this in more detail.

That might be described as “lack of choice” but it’s a strange use of the word “intrusive”. The point that I made earlier stands – private insurance, by the very nature of the way it has to work and its intrinsic objectives, intrudes between the patient and the doctor in a very perverse and potentially damaging way. It can literally dictate to the doctor what he may and may not do by withholding or limiting funding. The insurance company bureaucrat may as well be in the same room with them. Health care economist Uwe Reinhardt described this state of affairs as something that would be abhorrent to those accustomed to European health care.

But let’s look a little closer at this “lack of choice” aspect, picking up from what I said in the earlier post. It’s the nature of single-payer that coverage for medically necessary procedures is automatic and unconditional – the patient is not even involved in the monetary transaction. So if I can go to any doctor (or any hospital) I want, get whatever treatment I need that a doctor (not the insurer) deems necessary, and never see a bill – nor, in Canada, ever have to make a co-payment – what the hell more could I possibly want? So what is this “choice” thing about?

And there’s a beautifully ironic converse to that, too. Since all insurance companies have to make money (or at least break even) and all have the same expenses and follow more or less the same procedures, what exactly is the real meaning of “choice”? Sure, different companies and different coverages juggle costs and benefits in an infinity of different ways, but in the big picture what is really gained by going from insurer “A” to insurer “B” when providers and patients alike all get screwed more or less equally by all of them? Do you know how many complaints there are all over the Internet about exorbitant insurance costs, denials, and benefit cuts? Why don’t all these complainers just go from insurer “A” to insurer “B”?

I don’t have that choice and neither do most other people in this country. My employer makes the choice, and they make it based on cost, they don’t even know the particular needs of their employees.

That, too. This whole canard about “choice” is absurd. I would argue that if I lived in the US I would have no choice except to participate in the disaster of private health insurance, and pay through the nose for it.

Then your anecdotal experience is different than mine. There are several different plans available at my work and you can pick and choose which coverage you want. You don’t have unlimited choices, but within a give providers plans there are a lot of choices available. That’s been my experience pretty much everywhere I’ve worked…the most limited I’ve seen is perhaps a choice A coverage and a choice B coverage (and, of course, the choice to not take any coverage at all).

[QUOTE=wolfpup]

That, too. This whole canard about “choice” is absurd. I would argue that if I lived in the US I would have no choice except to participate in the disaster of private health insurance, and pay through the nose for it.

[/QUOTE]

Oh, horseshit. Good grief, why go to this sort of hyperbolic bullshit? Certainly there are problems with our health insurance system, especially for those who don’t have a full time job, but assuming you are working at a decent place your coverage and what you pay won’t be anymore than what you’d pay or get anywhere else in the world. Your only point to moan and groan and go into this sort of histrionics would be if you don’t have a decent job…THEN you’d have a point. But for the majority of Americans it’s not an issue…which is why it’s been so hard to ‘fix’. If it was the disaster you are making it out to be there would have been change by now.

This isn’t to say that it’s not important to cover the gaps and cover those who can’t get good jobs and good coverage through their jobs, or that costs, or that we couldn’t leverage what we currently pay to cover those gaps if we could agree on a system everyone could live with and pay the money we currently pay to the new system.

You said “the disaster of private health insurance”. That’s the hyperbole that is laughable. Agreed that lots of folks don’t like their healthcare/insurance. But something like 2/3 of the population are happy with their care. That’s far from a disaster.

Looking at the chart…yes, what you said is still hyperbolic bullshit. You are showing me that Americans overall spend more on healthcare. Knew that, thanks. We spend more on pretty much everything. But the individual burden for the average citizen is no more than what it is in most UHC or single payer health care countries when you factor in the fact we also pay less taxes. So, we pay more on the front end (along with the corporations and companies we work for who generally pay something like 80% of the costs) and less on the back end. Not seeing it as a ‘disaster’ or ‘pay through the nose for it’ FOR MOST PEOPLE. Do we get the biggest bang for our buck? Probably not. Is it the best system? Probably not. But it’s a good system for most people, which is why most Americans aren’t particularly riled for change. If you want to make a cast that we could get more, and cover more of the gaps for the same price or maybe a little more, that we’d be shifting costs really for most people from the front end to the back, well, I’d agree, and you can easily make that case without resorting to hyperbole.

They’re “happy” relative to what? Polls like that have limited value if the responders don’t have anything to compare their experiences to, or are unaware, say, of the economic impacts of the systems they are “happy” with. Even so, the percentage is much lower when they’re asked to evaluate the system nationally rather than their own personal experience.

With those poll limitations in mind, we can look at some other polls – here is a Gallup poll that asked exactly the same health care questions to responders in the US, Canada, and Great Britain. The responses:

Affordability – very satisfied or somewhat satisfied: US 25%, Canada 57%, Britain 43%; very dissatisfied: US 44%, Canada 17%, Britain 27% Quality of care – very satisfied or somewhat satisfied: US 48%, Canada 52%, Britain 42%; very dissatisfied: US 26%, Canada 22%, Britain 23%

Another poll showed that more than 86% of Canadians are in favor of strengthening the public health care system rather than introducing private alternatives, and that “most Canadians (85.2 percent) aged 15 years and older reported being ‘very satisfied’ or ‘somewhat satisfied’ with the way overall health care services were provided”.

Another perspective is personal and anecdotal, but an excellent comparison because it involves a family member who lived in Canada most of his life and then moved to a job in the US with excellent benefits and a first-rate health care plan. I asked his opinion of his US health care experience. Given the circumstances of executive-level compensation and benefits, he had no particular complaints about the health care services themselves, but was furious and endlessly annoyed at the insurance bureaucracy that both he and his providers had to put up with. That was his major complaint but it was a big one, and that’s much of what your insurance premiums are wasted on.

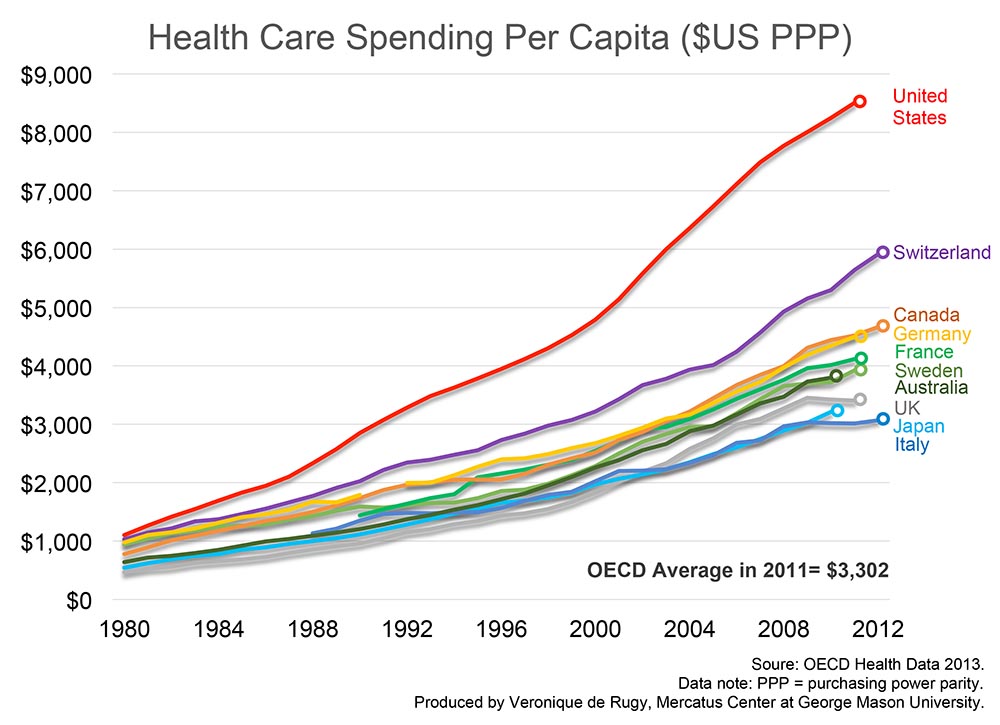

Costs are not just “more”, they are a spectacular outlier, more than twice the OECD average, and almost twice the per-capita cost in Canada. The “taxes” argument makes no sense; the health care costs are much lower, period, so if they’re paid via taxation instead of directly, it makes no difference – the net cost is still lower. Also, as I may have mentioned before, Canadian vs US tax rates are actually very similar, though there are enough differences that comparisons are difficult – low-income Canadians actually pay significantly less tax than low-income Americans, corporate tax rates are much lower, but high-income Americans benefit from more deductions. There is no way you can argue that taxpayers are somehow being gouged to pay for universal health care – the numbers just don’t stack up that way, and it’s an overall cost saver.

So you have much higher health care costs, yet you still have some 40 million uninsured, you still have health care costs as the leading cause of personal bankruptcies, even among those who thought they were protected by insurance, and, for many, you still have a feudal dependence on the employer for health care, so that loss of job can become tantamount to loss of health care and maybe loss of life. And in exchange for all that you get insurance bureaucrats meddling in the doctor-patient relationship and trying to block access to health care to improve their “medical loss ratios”. Is that a “disaster”? Well, the appropriate language is a matter of opinion. I’m sure that Bill Gates and those with secure jobs and good benefits think everything is just fine, especially if they falsely assume that the machinations of the insurance bureaucracy are just a fact of life and the same everywhere. But for many, it’s an intolerably bad situation.

[QUOTE=wolfpup]

Costs are not just “more”, they are a spectacular outlier, more than twice the OECD average, and almost twice the per-capita cost in Canada.

[/QUOTE]

Excellent…you should have no trouble, then, in showing that the individual burden on the average American is spectacularly higher than on the average Canadian, then. All you have to show is that the average American pays more in taxes and health care costs on a monthly basis than the average Canadian, and that this difference is so stunningly spectacular that it’s obvious to all. Showing me that the US pays more as a country does not demonstrate this, however.

BTW, on an unrelated side note, I lived in Canada for several years (Ottawa to be precise), and I can tell you that comparing pay stubs for like positions and salaries I wasn’t paying more but less than my Canadian counterparts when you look at taxes. Our take home was pretty comparable. Now, the case can be made, as I’ve said, that the Canadian’s get more bang for their buck and cover more with less overall, but from MY perspective I get as good or better health care and I’m paying about the same. However, this is obviously anecdotal, so feel free to back up your assertion and fight my ignorance. I’m serious…I’d really like to know this if you have the data.

Well, except I’m hardly Bill Gates, nor are the majority of Americans Bill Gates. The reason this hasn’t changed (yet) is that most Americans are relatively satisfied with the system we have and don’t really think about how we pay more and have more gaps than, say, Canada.

Seriously everytime the discussion turns to Canada I just stop caring. At. All. Good for you you like your system. I couldn’t give two shits about it myself but knock yourself out.

I am very curious as to what they were gaming the system for? I mean, what is the potential profit?

The US system would seem to encourage gaming or fraud far more heavily, as you have to pay for the provision of treatment, limiting provision and creating revenue streams that are easy to tap into.

But you do feel its the governments role to provide a basic education? A military for defense, police, courts, a lawyer if you are accused and cannot afford one, subpoena witnesses who may not want to appear, etc? What separates healthcare from the other duties of government if I may ask?

If you brought the country and population of 13th century Livonia under the Brothers of the Sword forwards to the present day, you might also find that they were on the average, happy with their health care. That wouldn’t actually make it any good.

If you spend a substantial amount of money on something, and don’t get value for it, its not good. When the US overspends on healthcare compared to its competitors by almost twice its military budget, and does not realize any competitive advantage, it can quite accuratly be described as “disastrous”.

Why don’t you?

I live in a single payer country, and its not the only one I’ve lived in. I’ve always had the possibility of going to insurer A or insurer B. Or pay out of pocket. The difference is that I’ve also been free to utilize a government option at no added cost.

You seem to be operating under the assumption that there are no insurers or private health care in single payer countries.

The entire worlds biomedical research budget is ~300 billion dollars.

The US share of that is about 130 billion, Europe accounts for about 140 billion. The rest is mostly East Asia. The biggest single contributor is the US government through NIH with 30 billion. Pharmas in the US spend about 40 billion, other healthcare companies roughly 25 billion.

For a period after WW2, the US dominated medical research, having both the money and an undamaged infrastructure. But this was based on exceptional circumstances, and for many years the US share of medical research has been declining.

The estimated waste in US healthcare -just the waste, not the whole budget- is 1200 - 1500 billion. That is 4-5 times the entire worlds research budget, and 40-50 times what US pharmaceutical companies spend on research.

A question for Bone and XT: what choice is important to you? I’m afraid I’m not following the argument.

If you’re living in a country where all medical procedures are covered if directed by a doctor, and you don’t have any premiums to pay, and no co-pays, and you never have to deal with the insurer, what do you want to choose between?

{kind=link}