No, I’m describing how a modern economy works, and pointing out that the empirical evidence is pretty damned clear that high taxation of capital leads to bad economic outcomes. I’m not the one simplistically assigning good and evil based on class.

A) no, they’re not. The vast amount of earned capital is re-invested in the productive economy. What do you think venture capitalists do? Where do you think Facebook and Google got their startup capital? How do you think Amazon paid to build its distribution network? Where do you think the money comes from that funds all those startups across the nation?

B) No, it’s not. Even capital moved offshore is being used to build offshore economies or to pay for offshore operations of domestic businesses. And the reason that money is parked offshore is because of the U.S’s crazy tax rules in the first place. There’s an easy fix for that.

Hey, strawman me some more.

Let me ask you something. The decision makers in a market economy are people with money. Lots of money, a little money, it doesn’t matter. If they can spend, they’re casting a vote of sorts. They’re voting for what gets made and what services get provided. If the money is concentrated in fewer and fewer hands, what do you think that does to the quality of the decision making? Because the Soviets had a rather small number of decision makers in their economy, and their economy was persistently stagnant.

If you think an oligarchy should be making most of the decisions for us, just come out and say so. Don’t feed us warmed-over Chicago school economics as if it’s immutable wisdom.

I’m sure it’s a simple matter to keep the capital around for your investments and to bring offshore money inshore for that purpose.

There’s a fix, but it won’t be easy by any means. Just enact a few laws with teeth in them that will put CEOs and accountants who hide money offshore IN JAIL. Don’t fine them, park their asses in a jail cell for a few years. The fines tend to be pocket change compared to the money gained by going offshore. But since both parties are owned by Congress, the prospects for that are dim indeed.

Minutes of research, however, gave me Forbes list of the 100 largest private companies in America. Two tech companies made the list. In Forbes “Global 2000” list of the top publicly traded companies, Apple came in #15, Microsoft #41 with almost all the rest being banks, petro or telecom companies. So maybe sometimes what’s right in front of your face isn’t the whole story.

Should be: both parties are owned by Wall Street.

Can you cite this please?

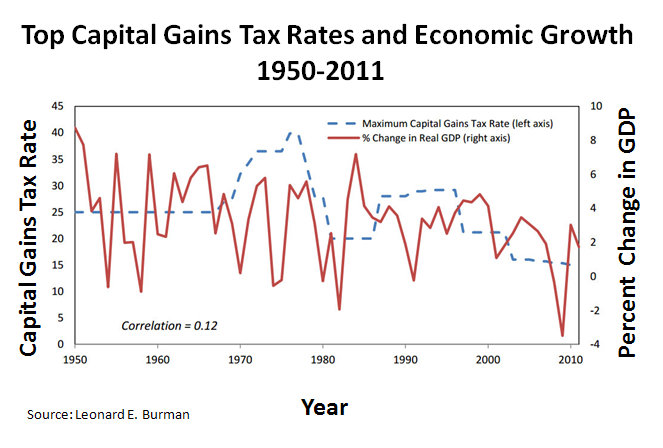

When I look at graphs like this one I am not seeing the correlation.

{kind=link}

I’m sure he meant it’s “pretty damned clear if you don’t look at the empirical evidence”. That’s what most “lower tax=good” people rely on.

For God’s sake. There is a ton of economic literature on the negative growth implications of higher taxes. I have posted such papers here many times. They fall on deaf ears because you don’t WANT to know about the empirical evidence. Your side would rather just demonize rich people and argue based on simplistic thought experiments or mutated, dumbed-down Keynesianism.

If you’d like some evidence, Here’s a paper describing the effects of Bush’s investment tax cut: The Bush Capital Gains Tax Cut after Four Years: More Growth, More Investment, More Revenues

Here’s a paper by Romer and Romer, discussing the effects of tax changes on economic growth: The Macroeconomic effect of tax policy changes

The abstract:

Bolding mine.

And from the conclusion of the paper:

By the way, one of the Romers is Christina Romer, the former head of Obama’s Council of Economic Advisors and one of the architects of the stimulus plan. No right-wing firebrand here.

Would you like some more? Let me know when you’ve finished reading and understanding that paper and I’ll give you more empirical data to chew on.

Because a single graph without context does not an economic argument make. You have to single out the effects of the tax changes from all the other things going on in the economy.

A major study that does just that is linked above. I suggest you read it.

Not only that, but the higher the tax rates, the more exemptions. I have serious doubts that the 40% tax rate applied to ALL investments. And also, wasn’t the income tax top rate higher during that entire period? So even in the days of extreme tax and spend, Democrats still saw value in keeping capital gains rates lower than income taxes.

From wikipedia:

Beginning in 1942, taxpayers could exclude 50 percent of capital gains on assets held at least six months or elect a 25 percent alternative tax rate if their ordinary tax rate exceeded 50 percent.[2] From 1954 to 1967 the maximum capital gains tax rate was 25 percent.[3] Capital gains tax rates were significantly increased in the 1969 and 1976 Tax Reform Acts.[2] In 1978, Congress reduced capital gains tax rates by eliminating the minimum tax on excluded gains and increasing the exclusion to 60 percent, thereby reducing the maximum rate to 28 percent.[2] The 1981 tax rate reductions further reduced capital gains rates to a maximum of 20 percent.

So when the rates were high, you could exclude a portion of it, which in effect meant the rates were only half that advertised. So even in the 40% days, they were actually 20%.

It also looks like Congress briefly experimented with high capital gains rates from 1969 to 1978, and I wouldn’t exactly call that a great time for the economy.

The difference is that the Dems are not wholly owned. Not quite. Yet.

We’re working on it. If the Tea Party keeps on pissing off K street, eventually they’ll decide to just buy the Democrats.

Sam Stone,

NCPA is not a serious research organization; it’s a libertarian think tank. That “paper” is crap. It lists a bunch of stuff that happens in the four years after the tax cut and assumes it was caused by the tax cut. Of course right after that you had the worst economic crisis since the Depression. Was that also caused by the tax cut?

As for the Romer/Romer paper I have patiently explained why it doesn’t mean what you think it means. As usual you are just cherry-picking the stuff that suits your ideology and ignoring the rest. For example their paper suggests that raising taxes to cut the deficit would increase growth. Clinton’s tax increases could be considered an example and since the US has been running deficits for more than a decade that is the part of their paper which is most directly relevant.

BTW an article on tax policy by Christina Romer:

I don’t need your ‘patient explanation’. I know exactly what that paper means - perhaps you don’t? As I recall, your last ‘patient explanation’ was to tell me that the paper wasn’t about stimulus spending - which I never refuted.

To be clear, what Romer and Romer did was try to find tax changes that were not a response to economic conditions (such as tax cuts during a recession to stimulate the economy). The idea was to find tax changes during an otherwise stable economy, so the effects of the tax changes could more easily isolated from other underlying economic changes, and would give us a better idea of what the effect of taxes really are. Other approaches in the past just looked at tax cuts or increases, and that risks confounding those effects with the underlying changes to the economy that were the impetus for the tax change in the first place.

Do you agree with that? If not, tell me where I’m wrong.

And yes, the paper also says that tax cuts that are applied to the deficit do not have the same growth-impairing qualities. I didn’t mention it because it wasn’t relevant to this debate. But since you brought it up… Doesn’t that suggest to you that deficits are seen by the economy as being equivalent to tax increases? If so, that kind of throws a whole wrinkle into the idea that you can stimulate the economy through deficit financing.

If not, perhaps you could explain the mechanism through which tax increases which are spent have a negative effect on the economy, while tax increases that pay down the deficit don’t.

And since you didn’t like my cites, here’s another for you:

Tax Structure and Economic Growth

The abstract:

Here’s another for you:

The Robust Relationship between Taxes and U.S. State Income Growth

The abstract:

Here’s a new paper from the American Economic Association:

The Dynamic Effects of Personal and Corporate Income Tax Changes in the United States

From the paper:

Would you like some more? I can probably come up with a dozen other peer-reviewed papers that find tax increases reduce economic growth.

Did you actually read that article? First of all, she’s talking about changes to cut the deficit - not redistributive taxes. Second, she fully admits in the article that tax increases can damage growth:

Bolding mine. So raising taxes through loophole closures would have negative effects, but not as negative as raising marginal income tax rates. She does not claim that tax increases can be made without harm to economic growth, and that’s using her assumption that the taxes will pay down the deficit. If they don’t, her original finding of major economic reductions still holds.

By the way, the term ‘tax expenditures’ as a euphemism for lowering taxes is not just Orwellian, it’s confusing. Democrats sure love to muck about with the language to mask the plain meaning of what they want to do.

But in any event, Since Romer is talking about deficit reduction, the article is a non-sequitur. We’ve already established that deficits are also destructive to the economy, and that the Romers found that tax increases to pay the deficit are not as destructive to the economy. But that’s not what we’re talking about here - we’re talking about straight-up expropriation of wealth, and not to pay the deficit but to redistribute to others.

And if you like that article, I hope you support this:

Among other things, she thinks high-speed rail should be killed, and farm price supports should be ended. I’m in total agreement with that, but most lefties are all for the high speed rail boondoggle.

4 fucking pages of comments about what an economist thinks. Really?

Economist’s opinion or flip a coin? Which would you trust? I’d flip a coin to choose which way.

Then you’d do considerably worse in predicting future events than those who, you know, actually analyze things. I realize that this is a popular opinion these days, but contrary to popular belief, economics is neither easy nor impossible, and actually having a clue what you’re talking about really helps you from falling into some very basic traps in thinking. The problems we’ve had in the economics profession have been failures of observation (people not understanding just how serious shadow banking was) and failures of application (people refusing to apply models that have proven themselves to work because it is politically expedient not to do so). The models themselves do a damn good job.

Sam Stone,

Romer/Romer is an interesting new methodology but some economists are skeptical that their division of endogenous and exogenous is that clear-cut, for example a good case can be made the early Reagan and Bush tax cuts were endogenous responses to a downturn.

Even if you take their numbers at face value the paper definitely doesn’t show that Keynesian fiscal stimulus is a bad idea particularly in an economy at the zero lower bound. Romer herself was a strong supporter of a bigger stimulus inside the Obama administration.

Neither does the paper show that raising capital gains taxes to say where they were 10 years back would damage the economy and as mentioned Romer supports increasing such taxes.

I am not still clear why you feel this paper supports your position. It’s an innovative method but not particularly radical in its conclusions. Economists have known for a long time that deficits can sometimes damage the economy and there are other papers which show that more persuasively than Romer/Romer.

As to the other paper first note that it’s from 1970 to 1997 and includes a vast range of countries including some poor countries that were basically socialist in the 70’s. It looks at a period where corporate tax rates fell from around 41% to 35 % on average and the latter number is still pretty high . Looking at the regressions I am pretty dubious about some of their controls; for example I don’t see oil prices or savings rates which had a big impact on growth rates in many of those economies. All in all it doesn’t show that corporate tax rates are too high in the US economy today or that an increase in revenue by closing corporate loopholes would damage the economy.

I don’t know why you think it’s a great revelation that Romer thinks that tax increases will have some disincentive effects. Most taxes have some disincentive effects according to basic economics. For that matter virtually every major industry has some combination of imperfect competition, asymmetric information and externalities creating some degree of market failure.

The trick is to figure which taxes have large disincentive effects and which market failures are large enough require correction.

If you have some papers which show that raising the capital gains tax to, say, 25% or closing corporate tax loopholes significantly damages growth feel free to share them.

So far you haven’t shown anything of the kind and really the kind of random crap you are throwing out like the NCPA article doesn’t inspire much confidence.