Okra and blackeyed peas seem to be the things that grow the best around here (Dallas) between July and September. Everything else seems to wither in the heat, or requires so much water that it starts to get expensive to keep them watered adequately (peppers, tomatillos and cucumbers specifically).

Everything else basically gets planted in the next few weeks and goes through mid-June, or gets planted in mid-August, and goes through about Thanksgiving.

I just saw a Boston Globe article about restaurants increasingly adding 3% or more “service charges” to the bill that supposedly benefit cooks and kitchen help.

Other such charges have been added for employee health care.*

I have mixed feelings about this. It’s great if restaurants are actually spending more to support workers. On the other hand, this seems like a ploy to guilt customers into not resenting menu price increases.

I’d rather they just raised prices to cover worker and other costs. If they want to boast how employee-friendly they are, print salary and benefit info on the back of the menu.

*next we’ll be seeing such surcharges on car repair bills and clothing purchases.

There’s a bar here in Dallas that did the same thing. And I feel a lot like you do- it’s great that they’re looking out for the workers, but it’s also kind of shitty to just tack on a 3% fee and call it out on the bill.

That’s not MY problem to fund their employee health care. I’ll just go somewhere else and save 3%.

They should probably just raise prices across the board by that amount and go on with business as usual. People are unlikely to notice that their pint of beer went from 6.50 to 6.70, and if they do, they’re likely to care less than seeing a blanket 3% fee tacked on to the bill.

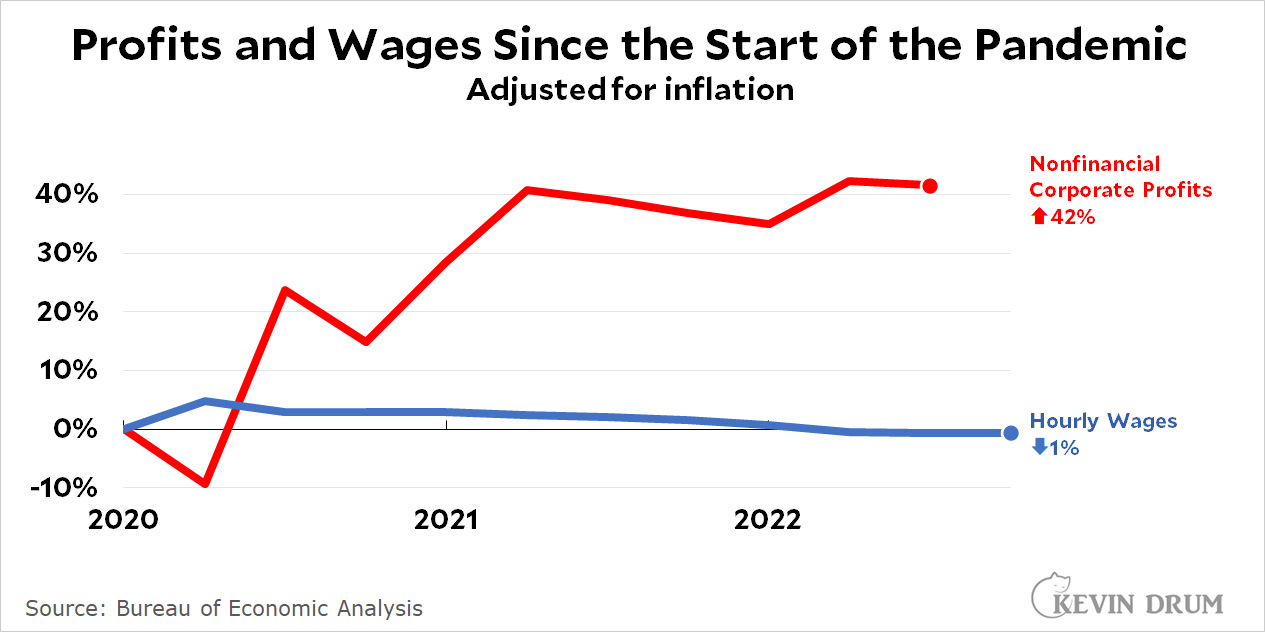

Neither of the graphs you show prove that to me, specifically for the issues I mentioned previously for restaurants.

The first graph shows total producer prices (the red line), and total producer prices, less food, energy, and trade services (the blue line). The legend mentions “food” and “energy,” but those aren’t shown on the graph you posted, and those are, IMO, the prices which have continued to be higher.

The second graph is for all industries, except for financial services. What do those look like (both profits, and wages), specifically for the food service sector?

Maybe they look exactly the same; maybe they don’t. But, you’re showing overall numbers, and assuming that they’re reflective, specifically, of what’s happening with restaurants.

Fair enough, and I don’t care enough to spend my day off doing work.

I’m not dismissing per se; I did say “Maybe they look exactly the same; maybe they don’t.” When you say, not just as a hypothesis, but apparently as a statement of fact:

…you’re making an assumption (which may or may not be accurate) that those broad cross-industry numbers are reflective of what’s happening in one specific industry.

But, because it was easy to pull, here’s your first chart, on producer prices, with the specific numbers for energy (bright blue line) and food (green line) turned on. You can see that both of those are trending well above the total numbers (red line), and continue to be high (even though energy costs are not growing as crazy-rapidly in recent months).

For January 2023 (the last month on the chart), energy costs are still +9% versus year ago (on a rolling 12-month basis), and food costs are still +12%.

Ah, thanks. I went digging for food PPI on BLS and didn’t immediately find it. That’s useful. 12% isn’t nothing, but there’s anecdata (yeah, I know) of 50% price boosts in this thread. My gut says it’s opportunistic, but my gut doesn’t beat your (or anyone’s) gut. And it was startling to see how little of these price boosts have gone to workers.

On that chart (from the link you shared), clicking on the items in the legend (food, energy, etc.) in the legend above the chart turns them off and on. (No, it wasn’t intuitively obvious, to me, how to do that!)

But, that’s not just 12% as a one-time growth; food prices have been growing at a 10+% rate for nearly 2 years – in digging into that chart, the monthly number has been +10% every month since June of 2021. The +12% as of January 2023 is compounded on top of similar price increases as of January 2022, as well.

The US does depend on both wheat and oil, so of course both are factors. When a commodity goes up in price, all of that commodity goes up in price. Maybe (probably) most of the US’s wheat doesn’t come from Ukraine, and most of our oil doesn’t come from Russia, but that doesn’t matter, because other parts of the world used to get wheat from Ukraine and oil from Russia, and so they’re buying wheat and oil from other places now that they didn’t use to, at higher prices. And so if we want to get those commodities, we have to pay higher prices, too.

That said, I suspect that for most restaurants, especially the cheaper ones, rising costs of labor are the biggest factor.

As for covid, according to actual epidemiologists, it stopped being an epidemic late last spring. The disease still exists, of course, but it’s no longer an epidemic.

That is not actually the way international commodities markets work. It is not the case that everybody pays the same price for a commodity; in many cases, developing nations that cannot afford even a marginal cost increase are simply priced out of the market which limits demand, or what surpluses are available are reserved for internal consumption and are never delivered to the international market, which is why nations such as China, which is heavily dependent on the import of perishable staple commodities, are trying to gain direct economic control over producers and logistics rather than depend upon the vagaries of market players. As @racer72 correctly pointed out, this has impacted natural gas because they have been importing it through LNG terminals that Germany constructed in record time; for oil while their was a jump in crude oil prices in early 2022 corresponding to the Russian invasion of Ukraine, prices have gone back down and stabilized at the pre-invasion level that they were at in the last quarter of 2021, and the rise before that was predominately the impact of increased travel and economic activity as nations and trade networks recovered to pre-pandemic levels of activity.

Regardless, the current inflationary cycle well predates the Russian invasion of Ukraine and is a result of the suppression and then prompt rebound of economic activity due to the pandemic, and the cost to restaurants is driven largely by labor costs and disrupted supply chains, not a loss of Ukrainian grain or Russian oil and gas.

Since your site is only the claim of nebulous “actual epidemiologists” it is any guess as to who you are getting information from. But while there is no explicit bright line between an epidemic and endemic phase, deaths attributed to COVID-19 are still routinely over 300 people per 7 day period which is well in excess of the CDC P&I threshold for influenza, and we’ve seen the effects of epidemic spread in China and elsewhere in late 2022. The most recent Omicron derivatives of BA.4 and BA.5, and the latter’s descendants of BQ.1 and BQ.1.1, while even more infectious than their antecedents do not appear to be more virulent, and the immunity of prior infection and/or vaccination does appear to have a persistent protective effect versus severe disease, so this may be an indication that these variants have settled down into a maximally infectious but relatively benign pathogen that will circulate seasonally or continuously with relatively little ongoing impact.

But no experienced epidemiologist is going to lay favorable odds at this point that a new variant won’t emerge that may have greater virulence, and I have discussed the issue with an epidemiologist and virologist working at a major research university who is convinced that a substantially more virulent variant will emerge based upon knowledge of betacoronavirus structure and how this virus has evolved in the past. We may be at the tail end of this pandemic or we may just be in a lull before an even bigger storm, and of course every epidemiologist is still waiting for the emergence of a highly virulent influenza strain that is what everybody was expecting when SARS-CoV-2 emerged seemingly out of nowhere. Which isn’t an argument for continuing lockdowns or other highly restrictive measures but it certainly does beg to sustain funding for both public health surveillance activities and the development of a general coronavirus vaccine.

The P&I epidemic threshold is literally the determining line between endemic and epidemic spread for influenza. There isn’t such a threshold for SARS-CoV-2 because we don’t have enough of a seasonal or annual trending history to develop such a metric. We may look back in a couple of years and decide that the epidemic phase ended in December 2022, or we may realize that we were in a several month lull before the emergence of a new variant that is highly capable in circumventing current immunogenicity. Making the definitive broad claim that “the pandemic is over” is not supportable on the basis of any current evidence.

Call it what you want, but nobody in the US or Europe (or I suspect most of the rest of the world) is treating it like it’s a pandemic anymore. No masking, no lockdowns, no social distancing, etc… Life is effectively back where it was in 2019.

I agree with you 90%, but if I’m out and about, even in California with very low infection and especially death rates, I see masked people every day in retail and other enclosed areas. It’s quite common (and perhaps required by law? Unclear) to see entire store staff masked, and I see everyone masked in medical facilities, including requirements for patients. Things are not back to 2019, but indeed less regimented than 2020. A 2019 person might be startled and puzzled at all the masks, even if it is now far from universal.

I actually still see social distancing in retail – people stand further apart, probably out of long habit. I kind of like it – stop tailgating me, shopper behind me!

I’ve been to Thailand this last December - I saw little masking outside of airports, but inside them it was expected (not required) but close to everyone did it. I still saw masks in town, mostly older people but not exclusively. You might see a young woman or a man masked just walking about outside or in a 7-11 or whatever. Masking is still a thing there.

I’ll be going to the EU soon, I’m interested to see what post-ish-Covid life is like.