I’ve recently been involved in a debate where someone told me that social security would fail anyway even it the income cap was raised. Now I’ve watched news programs that claim the opposite of that. This person also said that it would be generic me “taking and not giving” or some such and did I want to just take. Anyway, I would like to be informed if I debate this and I was wondering if someone would like to give the idiots guide to the income gap on social security. I can google it and I will but I thought someone here could explain it in simpler terms. Any takers?

There are a lot of statistical and actuarial assumptions built into all these debates. What will be the inflation rate for the next 20 years? The interest rates? What will or won’t Congress do on what timeline to who?

So I think truly factual (as opposed to merely plausible) answers are going to be hard to find.

The central point of course is that right now SS taxes are levied on “only” the first $160,200 of personal W-2 or pass-through self-employment business income. The technical term is the “Social Security wage base”. This levied separately per individual person in a multi-person household. So in theory, by simply raising that number you’d collect more tax.

But how many people (not households; individual people) in the USA have W2 above 160K? And how much above 160K? What is the size and shape and distribution of this potential SS revenue pool? That at least is a question for which round number factual answers are available to the experts with access to the data.

How many of these high earners are in positions where they can alter how they are paid to move more of their income into a non-SS eligible bucket like profit sharing or stock or …? That question is much harder to answer factually, as it is making a prediction about future public behavior in the face of changing tax law. CBO makes a lot of these sorts of estimates though and presumably has a rational experiential basis for doing so.

And how much of that extra revenue would need to be returned to higher-end recipients by also raising the eventual SS payout for those folks? That is purely a political question. Congress could do anything or nothing about that.

As noted above, the social security tax is only assessed on the first 160K of wage or business income. (The limit is adjusted upwards a little every year, I believe.) It’s been suggested that the limit be raised substantially or even eliminated altogether, in order to increase the revenue received.

The rub is that, under the current framework, the amount of money a Social Security recipient receives is based on the amount of money he or she paid in Social Security taxes while working. (Roughly speaking. The details are not for the faint of heart) So unless some other changes are made, the increased revenue from raising the limit will be offset by increased expenditure.

So possibly the answer is we aren’t sure how it would improve the trust fund, but it would improve it? And would the average SS recipient be “taking” from others? That’s the part I thought really sounded like bs, but didn’t have the expertise or even half-assed knowlege to debate it.

I am nonexpert here, but the whole “taking from others” thing belies a misundertanding of how SS works, AIUI. It’s not an individual’s bank account where the money you put in is given back to you in the future, it’s a pool of money that every worker pays into so that every worker gains some benefit in the future after they are done working. Of course if you receive the benefit you are taking from others - as you and I are paying into it as workers today such that others (retirees) can benefit today, we’ll be receiving the benefit when future workers are paying into it (when we are retirees). And yes, some put more money into the pool than others. Maybe I am not entirely correct, but I thought SS was designed that way.

will be partially offset by increased expenditure. And by expenditure occurring a long way in the future. So how partial is “partially” is TBD.

Then don’t. Most folks are utterly ignorant of how it works at a societal level. And you don’t need to know any of that to either pay in or take out. Most political “debate” is two people who know nothing arguing about stuff they don’t understand using terms they misunderstand. That’s a mug’s game.

Ultimately, SS is simply welfare by another name. Everyone pays some taxes and everyone gets some check. From the very beginning in the 1930s the government has tried to disguise that fact, knowing how violently allergic many Americans are to the idea of “welfare” even as they love cashing checks from Uncle Sam.

As @snowthx said, in no sense am I getting back the money I put in. Big picture I am getting money now from people paying taxes today and the money I paid in taxes 15 years ago was gone the very next day when SS sent it out to then-older grannies who’re now deceased.

Ordinary income taxes are “progressive”. Low-earners pay a low rate on their low income and high earners pay a higher rate on their higher income. This has the effect of flowing income and wealth downhill, partly offsetting the capitalistic system that flows income and wealth uphill to the already wealthy.

The SS tax is not progressive. Everyone pays the exact same flat percentage. Which changes from year to year, but is always the same for everyone at any given time. With, as said before, a limit that the tax is capped at being levied on $160K and applies only to wage income, not investment income. Most fatcats with real wealth get their income from investments, not wages.

Instead with SS the benefits are highly progressive. Assuming equal longevity, a lifetime low wage worker will receive total benefits far in excess of their total taxes paid, while a lifetime high wage worker will be the opposite: lifetime taxes will exceed lifetime benefits. Which, like the income taxes, has the overall lifetime effect of flowing income and wealth downhill rather than uphill. Of course some people live longer than others, and that factor tends on average to favor the well-off more than the low-wage folks, partly counteracting that downhill flow.

There are lots and lots of moving parts here. Any sound analysis needs to consider all of them.

Since there is exactly one large pot of money labeled “social security revenue and assets”, then any dollar paid out to anyone for any reason under any rule represents a dollar taken pro-rata from everyone else. “Taking from others” is a more or less meaningless sound-bite / hate buzzword, not a functional concept of how the system works. Like “woke”, it just stands for something / anything the speaker disagrees with.

Anyone using that term in connection with SS has loudly explained that they know just about exactly zero about SS. As bad as it is debating with someone when you know little to nothing, it’s far worse when they know little to nothing. You can only become stupider and less-informed by talking/debating with folks like that. Said another way:

The only way to win the game is not to play.

Yeah, I have little interest in debating something I know little about. I know that social security is not getting out what you paid in. I don’t think anyone needs to be an expert to know that; you just need to pay attention.This guy (and the nature of that site makes it difficult to return to the conversation) seemed to think that raising or eliminating the income cap would mean, we were taking from others and not putting in? Or something. He even asked if I wanted to only "take.

"I’ve done some googling, and I’m seeing a lot about the steep rise in income inequality has hurt the SS system. I think that is something that should probably be addressed. The political will for that is pretty weak though to say the least. The House is a joke right now and I don’t see that getting much better anytime soon.

A bit off topic but related: There are some real loons on that forum. One told that, “Barry” was running things, 'cause Biden is senile, and on the next line he was complaining about “the Biden crime family.” lol I told him he needed to meet us on earth one. That is why I wanted to check my assumptions about SS. I know that I’ve heard the income cap abolition would make things better, and it seems to me a cap is problematic; if everyone gets SS out everyone should be taxed on all of their income. However, as stated above I don’t know enough to debate it. I just thought that what he was saying sounded off, but couldn’t articulate to him why.

Another thing to remember is that SSI includes disability insurance. You’re paying in to get some support if you get disabled. Those who aren’t disabled should not expect (on average) to get out what they paid in (ignoring interest) because they “lost” that bet. Just as those who live a long time “lose” the bet with the insurance company.

From here in 2022 160k was in the 93rd percentile for individual earned income.

In my particular engineering field it is not uncommon to have earned income higher than this. I’ve hit the SS max for the past 30+ years. I’ve never been in a position where I can change my earned income into some other for of income.

One useful data point would be to compare Medicaire withholdings before and after the point when they removed the earnings cap (I think sometime in the aughts?).

I think it is less about the number of people but rather how much money is out of reach of the SS tax.

I suspect there is a LOT of money beyond reach of taxing for social security and a relative few who hold that money.

This discussion feels particularly acute to me as I will be one of the very first to lose SS benefits when I reach retirement. If they want to cut my benefits then just give me back the $200,000 or so I have put in (not gonna happen, I know).

@Marvin_the_Martian. Excellent info. I did not mean to suggest that 160K was some obscene or rare number number paid only to pro athletes; plenty of engineers, salesmen, and upper-middle managers make that. I too have been breaking the max for a very long time.

At the same time, 93% is roughly one in 12 workers. Out of curiosity I doubled the wages to 320K and came up with 98%. Which suggests that ~5% of workers are in that interval. Wherein if we doubled the cutoff from 160K to 320K, we’d capture SS taxes on anywhere between $1 and $160K of marginal income from each of those workers.

Even if we assume we got the full taxes on 160K (~=20K) each from all 5% of those folks, that still says each of them is only 1/20th of the total workforce, so the incremental $20K they contribute would be split amongst the benefits of ~20 total people. So an extra $1K/year/potential beneficiary collected.

But given the steepness of the income curve up there, there are far more workers in the 160-170K bracket than in the 310-320 bracket. So the average collected over the whole range will be WAG 1/3rd of what I just calculated, or about $300/year/potential beneficiary. IOW, it’d help, but it’s not some giant money fountain to solve all of SS’s funding and actuarial problems.

@Whack-a-Mole.

As long as SS taxes are levied on wage income, not total income, there’s not that much money up there. As I just demonstrated, even getting everybody up to 320K only gains $300/yr for everyone else. Going to e.g. 480K gets even less becasue although the dollars per head are more, the number of heads to tax is declining very, very steeply. I did not run that calc precisely because we don’t have data with enough resolution to know where the 87/98/99/99/5 percentile breaks really are.

Yes, there are a few e.g. pro athletes with W2 paychecks measured in millions. But they’re such a drop in the bucket of 135M-some full time US workers and another 100+M part time workers.

If we switched to levying SS taxes on interest and dividend and capital gains income, now you’d capture the serious billions and billions.

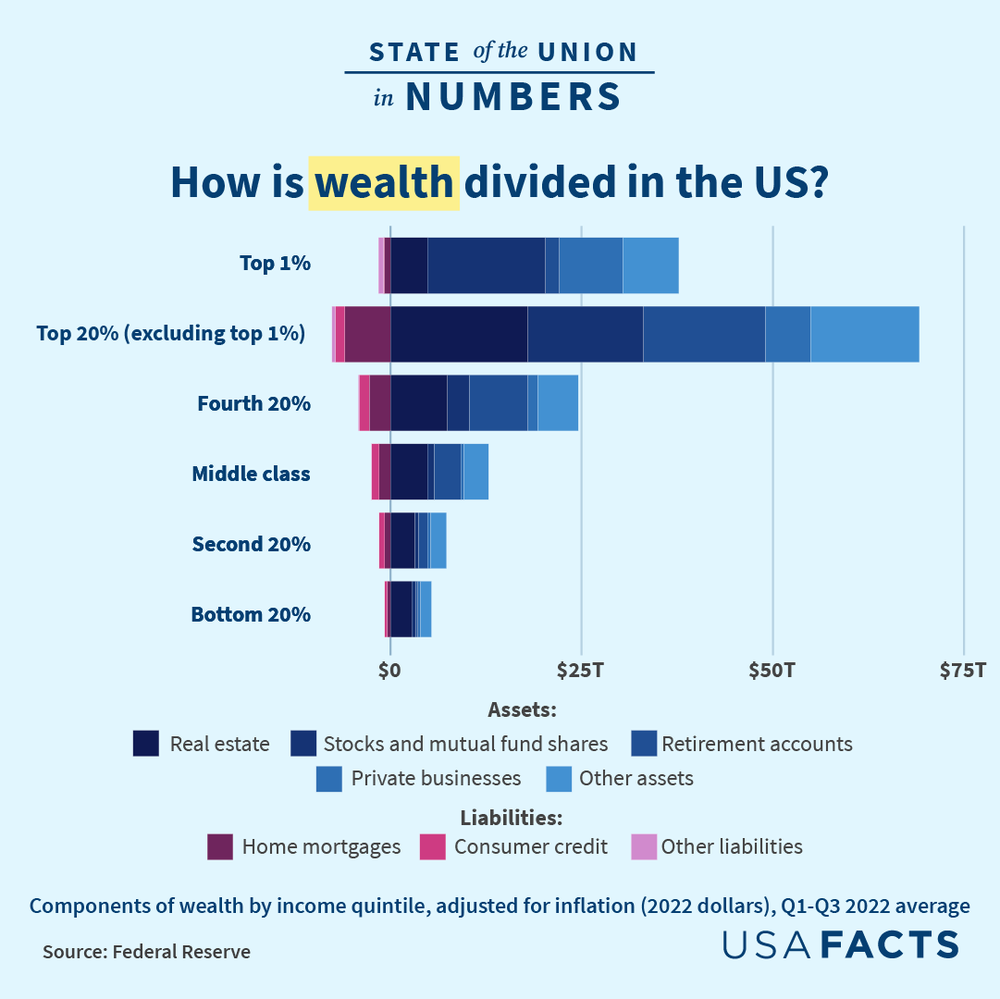

I think this illustrates the point. A LOT of money is out of reach of SS taxes. Middle class and below are supporting the system.

Income and wealth inequality are very real and very large. But since nothing about wealth is connected to SS, that graph is irrelevant.

If we want to have a totally different system where all forms of income (and maybe even all forms of wealth) are taxed to provide a living wage to elderly folks who don’t work, I’m all for it. But that’s no longer the US SS system. Which was always about wage earners supporting wage earners.

We are lightyears away from having the political will to support a UBI that works cradle to grave to ensure everyone always eats, has a warm (or cool) place to sleep, and can obtain quality medical care.

“Wage earners” is key here. So much wealth is not earned as a wage now. It is stock options and other tax dodges.

As I said, a lot of money is outside of this tax regime. Leaving wage earners (like me) screwed. I paid into the system (maxed it since my mid-20s…started in my teens). I did my bit for king and country. And now I am robbed of something I was promised at the moment when I need it. (I am not poor, I will manage fine, but I am lucky and I will say I will miss that promised income. Many are in a worse place.)

I too am a lifetime wage earner. I’ve saved some money and invested that both smartly and stupidly. In all I’ll be OK in retirement, SS or no.

I don’t know that we can say for sure that you or I or somebody 10 years younger yet won’t see what is currently promised. I would be more comfortable if demographics and funding were more favorable, but I’d be even more comfortable if about one-half of Congress wasn’t hell bent on wrecking the whole system in a fit of ideological pique.

SS is the best most highly progressive feature of our deeply regressive country. A low wage worker will be supported at retirement at 90% of their lifetime working wage in perpetuity. Somebody who earned and paid the SS max for their entire career will be supported at 25% of their lifetime working wage. Someone who made more wages than the max won’t pay more in tax but also won’t get more in support. Seems reasonable to me.

There’s the problem. About 2/3 of the wealth in the country is not taxed for this.

And yeah…I don’t get republican support when they are hell bent on wrecking the system. For another thread.

Wealth is not taxed at all in this country. Other than via real estate property taxes. Income is taxed. Yes, wealth generates income. And high income with the excess invested can lead to growing wealth. And existing wealth attracts more wealth over time.

Talking about increasing the wage income, or even the wealth-caused income, that is taxable for SS funding purposes is a vastly different thing economically, politically, and ideologically from taxing wealth itself.

It’s important to keep the various distinct ideas separate.

Why? Income is income. Whatever form it takes. Why should it be taxed differently? Why is one dollar in your pocket taxed but the next dollar isn’t? Why are those two dollars different?

I don’t mean to ride you on this…pet peeve of mine (and I’ve drifted far off FQ lanes so I will stop).

[Moderating]

A reminder to all that this is FQ. The numbers are facts. What the numbers should be is not.

@Whack-a-Mole I’m simply trying to keep income separate from wealth. The terms are not synonyms.

Wealth is what you own at a moment in time. Income is how much you earn over a period of time. Which earnings can be considered to include changes in your wealth. But does not necessarily have to include those changes if they are unrealized.

I’m speaking of conceptual accuracy and standard accounting. Not of ideology.