But you can’t just relocate to another country and expect them to pick up your medical needs willy nilly.

I cannot imagine it’s just that easy.

You know there is such a thing as medical savings accounts? The contingency plan should’ve been putting money into that. It’s a little late to be worrying now.

But they won’t quit trying to wreck it until they succeed. Any “replacement” that promises anything good will simply be a mirage that promptly collapses.

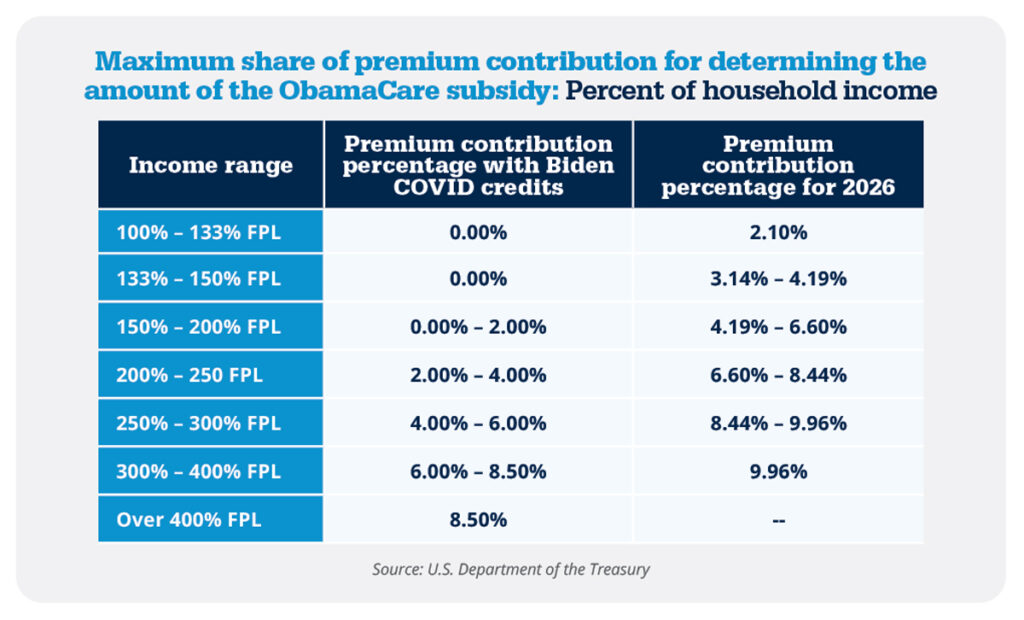

As others have said, the subsidies will not go away entirely. The ACA was designed with subsidies, but Biden passed expanded subsidies. The expanded subsidies will go away.

The original subsidies under Obama are in the right column, the enhanced Biden subsidies are in the left column. If the congress doesn’t pass enhanced subsidies (hint, they won’t) the subsidies go back to what they were under Obama in the right column. Subsidies don’t disappear completely.

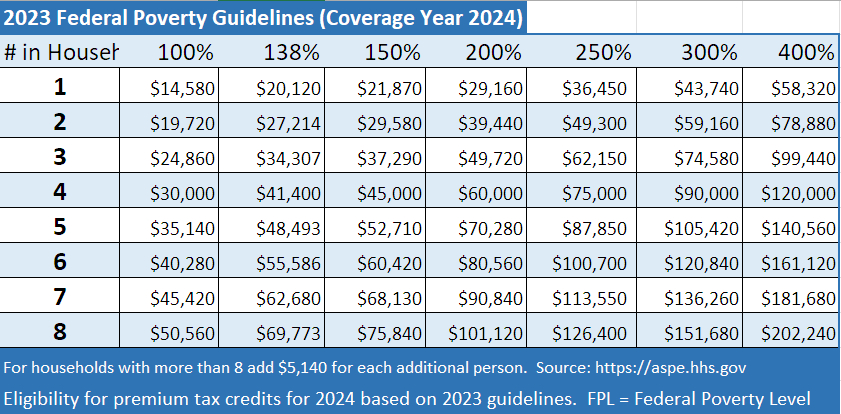

As long as your income is below 400% of the federal poverty level, hopefully the jump in premiums won’t be gigantic. Its the people over 400% who will suffer. In the original ACA, they got no subsidies but under Biden’s plan they were capped at 8.5% of income.

But someone with an income of 200% of the federal poverty level (FPL) will see their premiums jump from 2% of their income to 6.6%. If there are 4 people in a household at 200% of FPL (about 60k in household income) premiums will go from $1200 a year up to $3960. So an extra $2760 a year in premiums.

The problem is health care is a 5 trillion dollar a year industry, and any reform that truly reduces medical costs will cut into the business model and profitability of very rich, powerful companies. So nothing is really going to be done about this because any party that passes laws that reduce medical spending will see millions/billions spent on their opponents in primary and general election races.

Wow. Absolutely amazing. $10,320 per year for health insurance. I am gobsmacked

Here in the land up north, where we have UHC, and people tell us that we pay too much in taxes, Here’s what I paid last year on $66,000 income (very close to the average income in Canada):

Federal taxes: 4,294.70

Provincial taxes: 2,249.42

Total income taxes: 6,544.12

CPP deduction: 3,754.45 (not really a tax, equivalent to SSI)

Total taxes +CPP = $10,300

Convert to USD = $7,342.87

For this amount I pay, I get Universal Health care coverage for every citizen, I get CPP benefits at age 65 ($1300/month) as well as:

Citizenship and Immigration

Criminal Law

Competition

Copyright

Foreign Policy

Money and Banking (Bank of Canada)

National Defence/Military

National parks

Telecommunications and broadcasting (internet, phones & TV)

That’s because Obamacare is the Republican plan. They have somehow forgotten that. It was mostly created by the Heritage Foundation as an alternative to Hillary Clinton’s UHC proposal in the early 1990’s. Bill Clinton refused to seriously consider it since it’s really just a handout to insurance companies. But “HillaryCare” couldn’t get passed.

Hell, the GOP’s own presidential nominee implemented a version of the ACA when he was governor of Massachusetts. As a candidate, he had to disavow any recollection of that.

So, the Republicans have no alternative to Obamacare because they like Obamacare. IT’S THEIR IDEA! But, the Black guy got it passed, so…..

I’m not sure I agree with this foundation’s methodology of counting employer payroll taxes into an individual’s total tax burden. It seems to me that this should count as more of a corporate tax, rather than adding it to the individual tax burden.

But my point still stands - Our taxes in Canada pay for UHC. So you have to look at what you GET for that individual tax burden.

Trying to choose between healthcare plans here in the good 'ol USA reminds me of the Clint Eastwood dictum “Do you feel lucky punk?” I would gladly pay a premium in taxes to not have to do that.

Our premium just went up 30%. My husband is self-employed so it’s all on us. Last year, including premiums, we paid about $30k for health care.

I was hoping since my son no longer requires 24 hours of therapy a week the expense would go down, but with the price hike we’re looking at about $1600/month in premiums. $19,200 per year. That’s not counting anything we have to pay toward our deductible.

We are people who really need to use our health insurance, though. We couldn’t just go without. So we don’t really have a choice.

I don’t even think some Americans realize how expensive it is for some of us.

And the most outrageous thing is you pay thousands of dollars a year for health insurance and it’s fucking impossible to get them to cover anything. The hoops we had to jump through to get my autistic son services took hours and hours of lost wages.

Oh silly, that’s just the premium. You see, we pay that much just to be on the insurance plan – but of course the insurance doesn’t actually pay for our medical care just because we’re paying them that money in premiums. No, the person in question most likely has to pay around the first $3,000-7,000 of their medical care out of pocket before they meet their deductable, after which point they’ll continue to pay about 30-50% of the costs of their care. There are sometimes exceptions to this, for example some policies will cover basic primary doctor visits and preventative care for free, but for the most part you’re paying your premiums and still paying the first few thousand dollars of your care too.

So after that 20k in premiums and 7.5k in deductible, that’s when the insurance kicks in and you don’t have to pay… as much.

Even post-deductible it costs me $100/month to have asthma.

Our son’s out of pocket max is $9,000 (again, after premiums) and last year we hit it in May. We’re about $50 from hitting it again this year. That’s only for our son, see. Services for everyone else in the family still cost money. In total we’ve paid $14,000 and still have another $4,000 to go before we hit our family OOP max.

We really should be rioting in the streets but we’re all busy working to afford health care premiums.

Sixth bullet? ACA really sucks, at least if the goal was to direct more money towards health care rather than to further enrich insurance companies. Yeah, it is better for the uninsured than being uninsured. But no rational person/entity would think it anywhere near the top of any list of best ways to finance healthcare.

Yeah - all you folk in countries where you value the rational financing of healthcare, your mocking of our exceptional country is 100% warranted.

Jesus H. Christ on a pogo-stick. My “deductible” is … 0.

Of course at the moment, this does not include prescription drugs. For that, I’m on a private plan (extended health) which used to be covered by my employer, but I’m on my own now. For medical for a couple, that costs me $236.39 /month, 85% coverage for prescriptions with no deductible. Also gives me other stuff not covered by the provincial system such as convalescent care, OT, Physio, massage, podiatrist etc. etc. 80% to a max of $1300/year, vision testing, glasses ($400 every 2 years). etc . etc.

And if anyone wants to chime in about the horrible wait times in socialist Canada…

A few years ago my partner had a severe gallstone attack. Took her to emergency. She was admitted and on morphine within 60 minutes, scheduled for surgery that afternoon, discharged the next day (laparoscopic surgery is great). Cost to us… I think I paid $4.00 for parking, and bought a sandwich while waiting for $6.00.

No arguments about what was covered. Everyone involved got paid. Done.

That’s hard to even imagine. I think I paid around $3,000 to have my gall bladder removed. They tried to stick me with a $10,000 anesthesiology bill, but we appealed it. (This is a major issue in the US. Patient goes to a hospital that takes their insurance, finds out post-procedure that their anesthesiologist wasn’t in-network.)

But there are some areas where universal healthcare lags considerably.

I kvetched that there was a year wait-list in the US to get my son diagnosed with autism. The wait is excruciating. In places like the UK the wait is years longer.

Some children face even longer delays. Almost a quarter (23%) of those referred to community health services waited over 4 years (208 weeks) for an ADHD evaluation, while nearly 15% waited more than 4 years to receive an autism assessment

Four years is the difference, for some kids, between living independently someday, and not. Being able to communicate verbally, and not. It’s a really big deal to get autistic kids services as early as possible.

I think it’s further complicated by the fact that a lot of kids with less severe problems are waiting to get diagnosed than there used to be. Screening has become the default when it once was not. I don’t think health care systems are yet equipped to meet the new demand.

If you’re really unlucky, you’ll have just enough money to be above 400% of the federal poverty level, which means no subsidies in 2026. Then you’ll end up spending huge amounts of money on a bronze plan with a huge deductible.

Doing a quick run on healthcare.gov if you have a family of 4 (2 adults, 2 kids) and you make too much for a subsidy (if you make more than 120k a year in household income for a married couple with 2 kids) you are looking at about $1600 a month in premiums for a bronze plan with a $20,300 out of pocket maximum. Some of the bronze plans have a $20,300 deductible.

Some have a deductible closer to $10,000, but the plan covers about half of all medical costs between the deductible an out of pocket max.

But basically you’ll be spending 30-40k a year in premiums and medical bills before health insurance even kicks in on these plans on a household income of 120k, which after taxes is probably closer to 90k in net income.