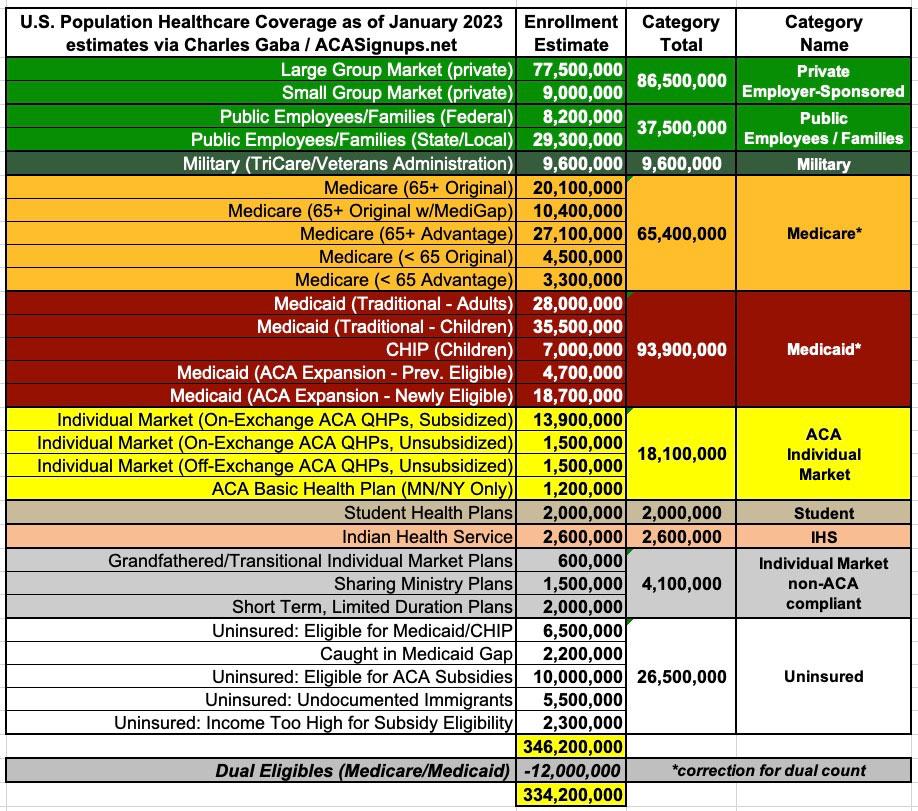

Charles Gaba has a blog that tracks the ACA and other coverage-related things. Just take a look at all the different types of coverage that people have in this link. It’s insanity on the scale of over 330 million people. He calls it the psychedelic donut, including the different types of Medicare, Medicaid, ACA individual exchange plans, ACA individual off-exchange plans, CHIP, VA, Tricare, Indian Health Service, Sharing Ministry Plans, Student Plans, Large Group Employer Plans, Small Group Employer Plans…and of course, the 8% of our nation that’s uninsured. It’s crazy.

I agree that this [non-]“system” is a disaster – it costs more than twice as much per capita than UHC in Canada and three times the OECD average while leaving over 26 million without insurance and putting everyone else through the grind of endless paperwork and risk of claims denial. I contend that this sort of thing is inevitable if you don’t have an integrated and well-regulated universal health care system, and the most efficient implementation of that is single-payer.

When the federal government forces everyone into one system, I worry about how well that holds up over time as the politics of the nation ebbs and flows.

I think private insurance schemes have been very helpful at times to help control costs, experimenting with networking, contracting, care organizations, and the like. It’s also allowed different employers to attract good employees. It’s different than just paying bills. Companies have come up with a variety of approaches that can help. And having private providers and insurers gives an opportunity for more experimentation, especially within different state markets.

If I were designing something from scratch, I wouldn’t have the US system. But it’s what we have, and I think it’s not as bad as people make it out to be. 90% of people are covered with something, and about 85% of them are happy with what they have. In any other issue, that’s a strong consensus.

Are you now more inclined to support some form of UHC?

My views have shifted a little. I’m not opposed to private health insurance (like the Swiss or the Germans or the Netherlands have). And I’m not opposed to having states do things differently to a point. But as we’ve watched the ACA play out, it hasn’t been strong enough to deliver UHC. The mandate was completely de-fanged. And the Trump administration undermined it. Biden has tried to make the changes that strengthen the law, and make it a better deal. But there are still 11 or so states that won’t expand Medicaid. There are still states that want to move away from the ACA. And the pandemic, in my view, laid forth the pitfalls that people can fall into. Some people get “insurance”, but still can’t afford their medical bills.

I think having too many ways to get insurance or to get “coverage” isn’t good. I think we need to move toward uniformity with something that is seen as a universal system. One reason that Social Security and Medicare are so supported, even by Republican voters, is that it’s universal for the elderly. Everyone is part of the system. That’s why SS & Medicare have more support than say, Medicaid, which is means-tested and not seen as “everyone’s interests are at stake”. So, I think that

My system would look something like the Swiss for the under 65 folks. Let’s call it “ACA On Steroids for All Who are Under 65”. But here’s where I’ve really shifted. If someone came along again and wanted to implement “Medicare for All”, I would be OK with it. We need something that is seen as truly national, and that has the backing of the people and strongly regulated. The current system isn’t delivering.

My shift in thinking has occurred during the last 3 to 4 years, and watching the pandemic unfold, and watching how the parties deal with healthcare and how different groups of people in the US have suffered.

Wolfpup - One other thing…I’ve traveled alot over the years to places like Japan, Singapore, France, Germany, Switzerland, Netherlands, and of course Canada (last year, we spent some time as tourists in Toronto, we liked the Hockey Hall of Fame…). No matter where you go, the people in those countries don’t worry about whether a medical emergency or condition will bankrupt them. They might have complaints about this or that in the system, but it’s not seen as an overall dysfunctional thing. But in the US, it’s a real problem. I know people who are middle-class, making around 100K per year, who skimp on health insurance because it’s so damned expensive. Our fragmented system makes this a real thing. I know people with full-time jobs that have no insurance at all. And at some point, we have to make the changes necessary to allow our citizens to move through life without fear of medical bills destroying their lives…

Damn, over 40 million people seem to have insurance through the ACA according to that. About 23 million via medicaid and 18 million through the exchanges.

If the US ever does get UHC it’ll probably be like the systems in the Netherlands or Switzerland.

It wouldn’t take much to get us to UHC. Just auto enroll all uninsured people into medicaid.

But uninsurance is just part of our problem. Huge issues with our system are things like it costs twice as much as any other system. Also we have huge issues with in network vs out network systems, plus insurance can abuse/mistreat customers by denying claims just in the hopes that people will just decide to pay. Also plans with huge deductibles aren’t really insurance anyway.

That’s the simplest and most obvious way to get a single-payer healthcare system, which is what makes the most sense. If we were creating a system from scratch (without all of the inertia from what existed before), and wanted maximum coverage for the least expense, this would be the best way to do it.

This is me. I’m not quite at 6 figures, but I’m going through a divorce and want to pay off my credit card and start saving for a down payment on a house. To do so, I stopped paying for health insurance, which is prohibitively expensive.

(Yes, I know the risks I’m incurring. I’ve made a decision based on the lost opportunities the expense is costing me)

I have said before and will say again: I relocated from the US to Europe for many reasons, but after years of experience the number one reason I will never return, by a wide margin, is health care.

Many Americans have a general sense they’re being ripped off. Few know specifically how extensive the ripoff really is.

I can attest to this. Canada has a lot of problems right now with too few family doctors, and long wait times at Emergency Rooms, but if you go to a ER with a major problem, you can still be seen quite quickly, and it won’t cost you anything more than parking fees, if that. I went to the ER in the middle of the pandemic with a serious breathing problem, and spent almost two weeks in the hospital as a result, and the only money I spent that whole time was on a few drinks from the vending machine, and renting a TV to watch some football games.

And even that is a generalisation, because of the provincial/territorial administration. Some areas have problems, but not others. In my city, even if my family doctor is not available, I can go to a walk-in-clinic and get medical care.

I am no healthcare expert by any means, but it seems to me that the only real issue with single-payer is getting people over the initial hump. Once it’s actually implemented, voters would eventually embrace it but the issue is that you can’t implement it without first, essentially, putting millions of insurance workers out of a job and dealing a massive blow to the pocket of BlueCross BlueShield, Aetna, etc. (if such companies would even still exist after single-payer.) They’d put up a huge political battle.

So it’s “no pain no gain” but no politician or party wants to be the “here, eat some short-term pain, voters” fall guy.

Yeah, this is one of the reasons I would prefer an “ACA on Steroids” as my UHC plan, just because I think politically “Medicare for All” isn’t doable. It’s hard to make a dent except incrementally in our political system. I’ll give Biden credit. He and the Dems greatly strengthened the subsidies in the ACA, and cleaned up some of the glitches that had previously existed. And it’s made a difference, as more people are signing up this year than ever before. However, to get the uninsured to sign up, you have to have penalties or auto-enrollment, which I don’t think our politicians will ever embrace.

I was in Europe last year, and another American I was with had to go to the hospital with some sort of bronchial/breathing issue. He was ambulanced to a hospital in France, and spent a night there. He got the care he needed, and then got out, and to my knowledge he didn’t pay a dime…

Back just before Biden was sworn in, I suggested that “Medicare for Most” should be the philosophy of his medical plans. The US already has a system in place for public funding of healthcare, the trick is to gradually get more and more people into this plan.

Step one would be to end the medicare/medicaid split. Because Medicaid is directed primarily at poor children, it’s an easy target for anti-welfare sentiments. Make it all one program, and make entry requirements for new kids as easy as it is for new seniors. Hopefully making it one program will reduce the stigma surrounding kids’ coverage. We can swing this as reducing the costs to private health care plans, because now businesses wouldn’t have to cover the employee’s kids any more. Cost Effective!

Step two would be to gradually make more and more people eligible for this new Medicare for Most plan. Reduce the age at which adults are allowed to join, and increase the age at which kids age out of the system. Over maybe 20 years, we gradually shrink the gap between these two coverages. Eventually we’ll have a kid born who loses the early age qualification the same day they qualify for the older age qualification, and at that point, private health insurance is no longer needed. The insurance industry has a couple of decades of gradually decreasing clientele, so have the time needed to gradually reduce their work force, or shift their business model to something sustainable under the new program.

Politically, I think this could be a winner. Voters in their 50s would see that every year we reduce the older age qualification puts them one year closer to not paying thousands for insurance, and maybe additional thousands for co-pays and “out of network” crap. Voters who just turned 18 will see that every year we increase the younger age qualification pushes back their own need for that kind of outlay. For people just starting their careers, this kind of economic benefit would be a huge improvement in their lives.

I was playing around with an online graphing calculator. Assuming we increase the younger age eligibility one year for every two years that passes, and reduce the older age eligibility the same way, a kid born the day the program starts would age out of M4Most when they turn 36, and age back into it at 43. That 7 year gap would suck for this person, but at the 47th year of this program, the young and old ages become the same. So kids born after the 6th year of this program would never lose their healthcare.

I’m glad to hear that your views have become more informed. The matter of private health insurance co-existing with a universal public plan is a fraught and complicated question, but the reality is that most countries do have such a system.

What I will say, though, is that comparisons with Switzerland or Germany can be easily misinterpreted. Switzerland probably comes closest to the US system because it leverages the private insurance system, but is still many miles removed because all residents have coverage, and the premiums are not risk-based. Still, the dependence on private insurance makes the Swiss health care system the most expensive among all OECD countries, aside from the US of course which is a complete outlier in its outrageous costs.

Germany is really quite different. The so-called statutory insurance scheme is a uniform and highly regulated system of private but non-profit “sickness funds” that effectively work like a single-payer system. The statutory system covers around 90% of residents, and conventional risk-based private insurance is used by only the wealthiest 10% or so.

IOW, the crazy, immensely complex and bureaucratic mess that is US health care exists nowhere else in the world. Even if there are sometimes superficial similarities, they turn out to be indeed superficial because everywhere else there is always a fundamental sense of guaranteed universal access to health care.

Yeah, Switzerland is more costly than other similar countries. But like you said, it’s the closest to our current system. So, I’d like to think we could politically get to something that approximates their model. In Switzerland though, the government will garnish your wages and auto-enroll you if you don’t get insurance. They take the universal part of UHC seriously, and the government will come after HC slackers. This is the part where the US fails completely, as we have no consequence for someone to not enroll in a plan via some means.

Yes, but in the states without the Medicare expansion, many people simply can’t afford to enroll in a plan. And even in states with the expansion, coverage can still be outrageously high. Our system truly sucks.

Yes, the Medicaid expansion was originally compulsory until SCOTUS made it optional for the states. So, there’s about 2 to 3 million people who are screwed by this, as 11 (I think it’s 11) red states won’t allow it, even though it makes sense economically and for the health of the citizens.

Buttigieg had a plan that was “Medicare for All Who Want it”…that might be a way to also gradually phase-in full UHC, as the government would allow it as a public option.

This is an important part, and relates to something that’s always bothered me about the discussion of universal health care. Our system in Ontario is the Ontario Health Insurance Program, but it it isn’t actually “insurance” as that word is usually understood. Insurance pretty much has to have risk-based premiums.

What we really have is a cost-sharing system. Everyone puts in the same amount (relative to your income), and then the government funds all the hospitals and doctors, and we all use the system as we need it. I think having the word “insurance” in there drives a lot of animosity, because people start thinking, “That guy who keeps breaking his leg is going to drive up my premiums!”, even though that’s not how it works.