Non of my facts have been refuted. You haven’t contributed much yourself, by the way. Instead of hiding behind the posts of others, why not take on my OP yourself?

I think this is a very sloppy argument. The definitions of Free Markets are abused constantly. Plus you haven’t provided any links to back up what you are talking about. It comes down to the difference between creation of wealth and redistribution of wealth. If governments destroy the incentive to produce and create wealth, they are redistributing a shrinking pie. Everyone gets poorer over the long run. What is wealth exactly?

Wealth is goods and services desired by individuals.

To think deeper about it though, businesses have to have a profit to continue doing business. This means providing goods and services to people that they actually want, at a price they want. What is a profit? A profit can be looked at in terms of goods. This means at the end of the day, one has produced more than one has consumed. If you spend all day laboring to produce two loaves of bread, and you eat both loaves of bread the same day, do you have a profit? No, you just have another day to live. If you spend all day laboring and you produce three loaves of bread, and only eat two, you now have an extra loaf of bread with which you can trade with someone else for something else, like a pencil. The next day you do the same thing, now you have two pencils Eventually you get enough pencils to trade for a chair or a piece of silver. Now, if you only produce 1 1/2 loaves of bread a day, eventually, you will starve to death, because you need to produce at least 2 loaves just to stay alive.

So, the reason governments do not produce wealth, is because they do not have profits. All they have are losses. They always need more money. The reason is twofold. First of all, governments are extremely inefficient. So even if they do produce a good or service that people want, they will do it so inefficiently, that they lose money, and as such, consume wealth by taking from wealth producers to fund their activities (for example, using the bread example, governments will only produce 1 1/2 loaves a day per person). Second of all, many goods and services provided by governments are not desirable. For example, licensing. If governments did not require people to get licenses to do business, no one would. As such, people have to waste their productive efforts buying worthless crap.

We want wealth to be created to improve the lives of everyone. The Socialist model simply fails in comparison.

Not just refuted, refudiated. You will never admit it, but it is clear to most readers.

Do you truly believe that the bailout money will be paid back? Did you know that the word gullible is not found in the dictionary?

The subsidies and bailouts are not related to the robbing of the poor and middle classes. ANY spending and creation of money by the Federal Reserve which creates inflation discourages savings and causes a redistribution of wealth towards the wealthy. But the rich get special treatment.

If we let the banks fail, the “worthless” assets would be valued in the marketplace and anything of value would be bought up by someone who is more competent. The bad debt would be liquidated, we would have a sharp downturn and we would go back to work. In a couple of years we would experience a robust recovery.

There is an excellent article by Nathan Lewis on the Huffington Post called:

What Happened to the Middle Class?

Here it is:

**In the 1930s there was a debate about whether to use currency manipulation as a means to help the economy. On one side of the debate was the classical economist, who said something like, “In the long run, you can’t devalue yourself to prosperity.” On the other side was the Mercantilist or “Keynesian” economist, who thought that a currency devaluation would help in the short term. The long run was not a concern of the Keynesian. Keynes himself argued that “in the long run, we are all dead.”

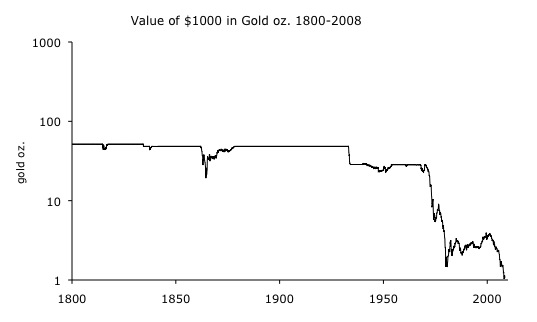

Politicians found the Keynesian stance persuasive. In 1933, the U.S. dollar was permanently devalued for the first time since the establishment of the United States in 1789. Its value fell from $20.67/ounce of gold to $35/oz. As is often the case, this indeed seemed to help, and the economy staged a recovery although the Great Depression continued on until 1940 and arguably until 1949.

In deference to the classical economist, however, the dollar remained pegged to gold after its one-time devaluation, and remained pegged to gold at $35/oz. until 1971.

Previously, we examined the history of the U.S. dollar. The “dollar” actually dates from 1513, as a silver coin made in Germany. The U.S. adopted this standard in 1789, and maintained it until 1933.

During the 1950s and 1960s, the dollar remained pegged to gold at its 1933 rate of $35/oz. These were wonderfully successful decades for the U.S., and the middle class reached unprecedented levels of prosperity. We can see here the floating currency system that was introduced in 1971.

This is an inverted logarithmic graph, to show a decline in dollar value as a move in the downward direction. At $20.67/oz., $1000 was equal in value to 48 ounces of gold. Today, $1000 is worth about 0.8 oz. of gold.

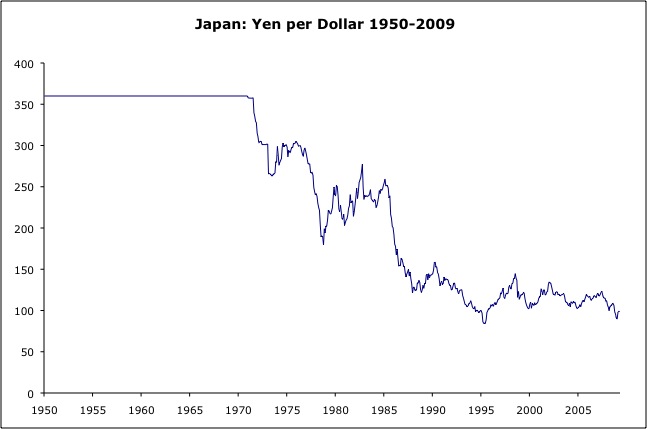

During the Bretton Woods era (1944-1971), all major world currencies were pegged to the dollar. They didn’t float. For example, here is a chart of the yen/dollar rate, which shows that the yen was pegged at 360/dollar during the Bretton Woods years.

However, the Keynesian money-manipulators were gaining influence. They envisioned a system where the government would “fine tune” the economy on a continuous basis, through interest rate and currency manipulation. This system appeared, as something of an accident actually, in 1971. Since 1971, we’ve been living in the Keynesian’s world of floating currencies. The classical ideal of a stable currency - a currency linked with gold - which worked so well for most of the U.S.'s history, sank into the background.

The classical economists warned that any system of currency manipulation would prevent long-term prosperity. You can’t make people wealthier by jiggering the currency. Prosperity is built on the foundation of a stable currency, which always meant a gold-linked currency.

Indeed, we find that the U.S. middle class’s long path of success ended precisely when the classicals’ gold standard system was replaced by the Keynesians’ floating-currency system in 1971.

You can look at the same thing in terms of ounces of gold. Remember, a dollar was worth 1/20.67th of an ounce of gold for most of U.S. history. So, if a worker earned “$100 a month” in those days, in the 1880s for example, that meant about five ounces of gold. They were often literally paid in gold coins. (Five ounces of gold today are worth about $6000.) During the 1960s, “$100 a week” meant about three ounces of gold. How many ounces of gold does a worker make today?

This is a graph of wages for “production workers,” excluding management and income from capital. Can you see why it now takes two “production workers” per household to earn what one did in the 1960s?

This is not the only problem facing the U.S. middle class. The healthcare system has become little more than a system of extortion, and the labor/capital ratio has been badly skewed by the introduction of huge new labor pools in Asia.

However, I think that a stable currency system will be necessary if you want to return to the level of economic health we had in the 1960s - the last time we had a stable currency. Otherwise, in the long run, “we are all dead.”

**

A combination of reckless monetary policy and government programs like Fannie Mae and Freddie Mac combined to create an artificial boom which inevitably leads to a bust. Alan Greenspan lead the charge with extremely low interest rates and reckless monetary policy in the 80s and 90s. There was the creation of too much malinvestment, which Austrians know, causes a crisis to be inevitable. Listen:

The value of a prices is that they provide signals to market participants: when, where, in what quantity, and towards what ends should investments be directed. These signals are valuable information that market participants use in directing the resources at their disposal. Cash, credit, finished products, works-in-progress, etc. Any interference with prices, therefore sends inaccurate signals to investors, entrepreneurs, consumers, borrowers, and lenders.

When money is injected into the system, it causes prices to change without a corresponding change in time preference which would be necessary to meet the “demand” contrived by the inflation. The takeaway here is that if time preferences haven’t changed, fiat injections cause a disconnect between prices and time preference.

New money, especially fiat money, typically manifests itself as demand for consumption goods. Keeping in mind that “consumption” is just a polite and roundabout way of saying that you’re destroying something valuable, since this consumption wasn’t matched with a previous investment in productivity, it’s likely to be a net value destroyer.

What happens when new money is introduced, is that demand appears to have increased, manifested by higher prices. These prices tell people “make more stuff”, this is how it works: People see a higher price being paid for certain goods, and this appears to indicate that there is perhaps profit to be made in that market. Responding to the apparent signal, they begin now to overwork their assets, or perhaps to invest in assets that will enable them to be more productive tomorrow.

What has not changed is the present productive capacity.

Prices rose, however, because of the money; the higher prices being merely reflections of the increased money supply, and not of any fundamental change in consumer preferences. This money eventually works its way through the system, and people discover that they over-utilized their productive assets yesterday (and therefore can’t produce as much today) or that they invested in assets in an attempt to match increase capacity to accommodate a phantom increase in demand. When this fact is eventually revealed, many investments are revealed as unprofitable and must be liquidated, and in either case we are worse off.

It requires previously accumulated capital (higher order goods) to facilitate the production of more consumer products (lower order goods) without depleting the existing capital stock. In order to have more today, it is imperative to have invested in productivity, made some sacrifice towards that end, yesterday.

This process does not work in reverse.

Without that previously accumulated capital, a boom/bust phase is inevitable.

I have been diligently working through this thread, putting significantly more energy into my responses than most of you. Dismissing something because the economists are “generally considered to be kooks by mainstream economists” undermines your credibility. I have responded with great detail to many posts here. It is hard to undo the misconceptions many of you hold and distilling all that I have learned through several years of study in a small post. To really understand some of this stuff, you would need to actually read some of the literature, and I am sure non of you will do that.

If you claim that people like Mises, Hayek, and the great classical economists are kooks you should answer this question (that I have posed over and over, without a response):

**Why have the Austrians been right in their predictions of this current crisis (not to mention many others over the years) while your beloved “mainstream” economists, with few exceptions kept claiming the economy was strong in 2006, 2007, and 2008? **

Maybe, just maybe, Keynes and his successors were wrong and their are timeless truths that the classical economists knew that have been ignored in recent years? Can you accept that possibility or are you to close minded?

Frankly, even if I hadn’t read everything about Austrian economics, I would look at the track record of the Keynesians and “mainstream” economists and be willing to try anything different.

What makes your brain think that freedom and lack of debt and an economy based on savings and production equates to lack of “progress”?

The idea that with a 100% reserve standard there can’t be loans is nonsense. There is a difference between DEMAND deposits and TIME deposits. It is TIME deposits which get loaned out. As long as you have savings, you can loan it. In a 100% reserve system, depositors would not make interest and would instead pay for the storage space.

Seriously, do you just shoot off at the mouth without actually looking into what I am saying? If I were you I would refrain from that sort of thing, unless you want to make yourself look like a fool.

Not all of them. There could be commodity backed currencies that get circulated domestically. Whichever one tends to maintain its value and purchasing power over time would have the most appeal to people.

No, actually I have failed to distill all the Austrian literature on this thread. :rolleyes:

You should look through my links. It seems to me you are intentionally putting your head in the sand because if you look too hard at what I am saying, you will be convinced, thus conceding the debate. Don’t let pride get in the way of your personal growth as a human being.

Good grief…that’s…well, completely insane. I wouldn’t even know where to start on something this loony.

-XT

[/QUOTE]

I find it pretty humorous how some of you respond to anything that refutes your favored Keynesian paradigm. Instead of reasoning and intellect, you label things “loony” or “insane” or any other derogatory comment.

So, xtisme, I want you to very clearly articulate why a system like I proposed, which the Constitution mandates and the Founders endorsed, is foolish and the effects it would have. Granted there will be a sizable challenge to get from the system we have now to that system, but once the transition is made, what are the downsides to an economy with little to no debt, with stable or appreciating money?

I am waiting for your response.

And I am awaiting word as to where and when that integrated Tea party rally took place.

Well, I’m glad you agree that I am “probably” not a racist. I am not really going to focus on this point, but why don’t you consider how the many people who are concerned ONLY about the economy feel when they are labeled racist in the media? If a majority are not racist, then it is wrong to label them as such.

The truth is, there are many conservatives in this country who protest more when a Democrat is president, regardless of skin color. Perception is reality to many people. The perception is that the democrats are the big government party and favor out of control spending and the republicans are “fiscal conservatives”. As you know this is complete bullshit, but many conservatives have a total blind spot for fiscal issues when Republicans are in the White House. This would be the same if Hilary Clinton was president.

The Libertarians are the ones who criticized both parties equally for the deficit and spending problems. They are the ones with integrity and principle on this issue. From my side, I am glad some conservatives are on the bandwagon now, but I agree they are hypocrites.

The truth is the Tea Party started in 2007 in support for Ron Paul. It was clearly even more anti Republican then. People thought Hilary Clinton was going to win. Yet they still sent Ron Paul 4.5 million dollars on a single day, and then 6.5 million on the anniversary of the Boston Tea Party. That is the roots of the libertarian protests that I support.

As I stated earlier, the definition of inflation is skewed. Inflation is not an increase in prices, it is an increase in the money supply. Rising prices result from inflation. From Mises.org:

http://mises.org/daily/908

Its common sense. What does the Fed generally do, year after year? Creates money. THAT IS INFLATION! It does more than that to be sure, but that is the primary function of the Federal Reserve. Now, the government won’t phrase it that way. It will say it is providing “excess liquidity” or “monetizing the debt” or other cryptic saying that most people don’t understand. By its very nature it creates more inflation year after year.

Nope. You are the one who is misinformed. It comes down to the true definition of inflation. The fed doubled the monetary base since 2008. That, by definition, is very high levels of inflation. These reserves are sitting on the banks balance sheets, not being spent into the economy. So, prices haven’t risen yet. Rising prices is a result of inflation, not inflation itself. Thats why they claim we have deflation at the moment. I have already posted a ton on this subject. Read up.

You have to fix the value of the money supply to a commodity, but it certainly doesn’t kill the growth of the economy and personal wealth. The economy grows based on production and business expansion.

Yeah, we have gone over it before. I’ll recap:

The things Ron Paul has been right about:

The war in Iraq and its consequences

The war in Afghanistan and its consequences

He predicted increased terrorism as a result of 90s era foreign policy (then 9/11 happened)

He warned about the current economic crisis for nearly a decade before it happened

There is plenty more.

Aren’t these the really big ones though? Many that you may label as “wrong” are really long term predictions that haven’t come true yet.

I am not saying he never gets anything wrong, but his track record is better than 95% of politicians and forecasters.

There is so much wrong here. I know you can BUY gold, I’m not talking about that. I’m talking about fixing the value of gold to the dollar. If the dollar is continually being depreciated against gold, they don’t care if you buy gold. But if the dollar is pegged to gold and you trade your certificates for gold from the government it provides a system of checks and balances that keeps the government in check.

Obama is warmongering and constitution shredding? You should be disgusted at Obama himself.

If you want to be critical of ME, however, you had better know what the fuck I am talking about. I can’t make you have an open mind. I can’t make you read books and study economics. But I hope more of you wake up before it is too late.

No, you’re wrong, and so is Ron Paul:

[quote=Ron Paul, 2002]

[ul][li]an oil boycott will be imposed[/ul][/li][/quote]

Wrong.

[quote]

[ul][li]The Karzai government will fail, and U.S. military presence will end in Afghanistan.[/ul][/li][/quote]

Wrong.

[quote]

[ul][li]a major war, the largest since World War II, will result.[/ul][/li][/quote]

Wrong.

[quote]

[ul][li]The draft will be reinstated, causing domestic turmoil and resentment. [/ul][/li][/quote]

Wrong.

[quote]

[ul][li]Many American…civilians will be killed in the coming conflict.[/ul][/li][/quote]

Wrong.

[quote]

[ul][li]The leaders of whichever side loses the war will be hauled into and tried before the International Criminal Court for war crimes.[/ul][/li][/quote]

Wrong.

He further stated to keep these predictions around for “5 to 10 years”. This was in 2002. Unless you think all of the above will take place in the next 2 years, you have to admit that Ron Paul is wrong. Until all of the above take place, you have to admit that, at the very least, Ron Paul was not “spot on” with his predictions.

The draft, oil boycott, mass civilian casualties, ICC war crimes - these are most certainly not “long term predictions.” Further, terming things as such is a cop-out: certain predictions will always come true over the long term, and referring to them that way reduces the usefulness of the predictions to zero.

Just admit you were wrong. The facts are quite plain.

Considering your penchant for writing at length, I’m surprised a mildly complex sentence like Inigo’s got the better of you. There’s a word at the end you missed.

I understand Austrian School economics. I have studied the philosophy and predictions of:

Carl Menger

Ludwig von Mises

Friedrich Hayek

Murray Rothbard

Hans-Hermann Hoppe

Friedrich von Wieser

Jim Rogers

Hans Sennholz

Ron Paul

Peter Schiff

I have witnessed the correct predictions of the Austrian School with my own eyes. I understand the monetary system and the way the Federal Reserve System benefits private bankers and is an attack on freedom and fiscal well being for our country.

Do you simply worship at the alter of Keynes? John Maynord Keynes 24/7? Everything outside your limited bubble is crackpot bullshit, I guess.

Yes, but certain economic systems allow for the least number of poor and vulnerable. Free Enterprise, Private Property, and Honest Money is that system. If you care about the poor, you first want to endorse the economic and government system the allows for the maximum prosperity for her citizens and the least amount of poverty. You claim there was no anti poverty program before your hero FDR came into office? I recall a speech given by Lawrence Reed, president emeritus of the Mackinac Center, for Grove City about what the government can and cannot do to help the poor:

Welfare statists make a crucial error when they imply that it was left to presidents of a more enlightened 20th century to finally care enough to help the poor. The fact is, our leaders of the 1800s did mount a war on poverty — the most comprehensive and effective ever mounted by any central government in world history. It just didn’t have a gimmicky name like “Great Society,” nor did it have a public relations office and elitist poverty conferences at expensive seaside resorts. If you could have pressed them then for a name for it, most if not all of those early chief executives might well have said their anti-poverty program was, in a word, liberty. And it meant things like self-reliance, work and entrepreneurship, civil society institutions, a strong and free economy, and government confined to its constitutional role as protector of that liberty by keeping the peace.

We have strayed so far away from these principles that generations are not privy to the experience of true prosperity and social justice that liberty and private property allow.

You think I have studied economics for years, yet somehow missed the concept of “supply and demand”? :rolleyes:

There is so much missing in your argument. The point made by the welfare statists is that the market is not “moral” so we need government involvement. But people (some of them) are moral. Now, if people are very wealthy and are not taxed to death and have excess capital, they are much more likely to reach out and help someone who needs help. Private charity and individual involvement in providing social aid or assistance is much more effective than government coercion and impersonal wealth redistribution.

In a free market, competition drives down prices. In truth, even today in a certainly less than optimal market conditions, the necessities of life are available to nearly everyone. Unless you are mentally handicapped or have a drug addiction, no one is going to starve. In a true free market products considered luxuries just a short time ago become available to nearly everyone. It is the industry of scale that markets provide which lowers the cost for goods and services and raises the standard of living for everyone.

Now, government is truly immoral. If your criteria is morality, the last place you should look for help is government. Governments steal, start wars, spy on their citizens, torture, conduct medical experiments on unsuspecting citizens, take away our liberties, and even imprison us indefinitely without trial. That is what goes on today. The market is nobody, its an abstract concept denoting free people peacefully engaging in voluntary transactions.

I would take that any day over authoritarianism.

No they don’t. Wealthy people who really want to help the poor or combat a social problem create charities and actively get involved in helping people themselves. They volunteer their own time. They don’t steal from other people to give the money to what they consider a worthy cause. And the wealthy that run charities are orders of magnitude more efficient and effective than government handouts and assistance.

Socialism destroys the incentives for production. It lowers the standard of living for everyone. Hating people merely because they are rich is a childish level of jealousy that no adult should engage in. If a person makes his money providing value to other people, then he is worth that much. Redistribution of wealth does not work at eradicating poverty, it merely makes everyone poorer over the long run.

And, although I have made this point before, it doesn’t seem to be sinking in. Even if you want government to have all these social welfare programs, there is no ability to fund them. Period. Which brings me to:

Where did you study economics? What were your textbooks? Who was your professor? What, by the way, about my adopting of “Batshit-Insanonomics” leads you to believe that I don’t understand supply and demand curves? Even your ridiculing of the great Austrian intellectuals and proponents of liberty says more about you and your childish name calling than besmirching the achievements of the scholarly works of liberty over the ages.

Yeah, you learned Keynesian economics, and I have spent much of this thread explaining why Keynes was wrong. His theories were very convenient for the bankers and politicians who wanting to intervene in the economy and grow government. That is why Keynes became the “standard” in the mainstream, not because of his prescience or validity of his theories.

It is impossible to give a precise date. The Austrian economists know that there are too many factors at play. The predictions are accurate but the timing can be difficult to determine. The economists who are thinking along these lines believe that it could happen in the next five years. If we don’t change policies and deal with our budget deficit and spending binge it will certainly happen within ten years. That is what I am hearing. We cannot predict what schemes our government will come up with. They could delay it for a while but the writing is on the wall.

I linked to that to show the countries that have experienced the worst cases of hyperinflation. Fiat currencies don’t last. They are not guaranteed to create hyperinflation. They can end voluntarily when a fiat currency is replaced in some cases. There are ALWAYS negative effects however.

I didn’t link to that to prove that fiat currencies are guaranteed to hyperinflate. I could have chosen other links for that.

I never said government debt couldn’t come down in the absence of a gold standard. Where did you get that idea? I am saying that a gold standard or other commodity standard is a proven way to maintain the value of the money and simultaneously keep in check government power. That is all.

By the way, does anyone looking at Canada’s debt stunned by how small it is compared to the United States? Canada has a national debt which is the same as the price of a three bedroom, two bathroom home in California? Don’t ever compare this kind of country to one with a thirteen trillion three hundred billion dollar national debt and claim they are similar.

Yes, under any system there are goods and services that some people cannot afford. Is this supposed to be some profound point? So, I guess its the governments job to give everyone something they can’t afford on their own?