It was a regular full-service bank, not a credit union or a savings and loan, in one of the Chicago suburbs.

I did banking in southern states before integration, but I can’t really remember such details. But with few exceptions (lodging, food service, etc.), all businesses were open to blacks, who were free to go inside and conduct any legitimate business, and would be waited on with a modicum of courtesy by white clerks. Highly variable from store to store, or course, and blacks knew from experience what kind of a reception they would get from any particular merchant.

In the case of a bank, it is very possible that they had a “colored window”, where black patrons could access a teller, so they didn’t have to stand in the same line.

Before about 1960, it was pretty unusual for a worker to get a paycheck. More often, it would be a little manila envelope with cash inside, with stub information written on the outside of the envelope. So a black worker who received wages would not, for that reason alone, have any need to go into a bank. I don’t think I ever got paid by check in any of my jobs 1955-1961. Not even on-campus jobs for which I was paid by the university bursary.

My father did not have a bank account until about 1950. He didn’t have enough savings to matter and checking accounts required a minimum (probably several hundred dollars) that he could not maintain. He paid bills either at a bill paying service a couple blocks away or by getting a money order at a bank.

He got paid by cash every Thursday. Until one day there was a holdup and the company arranged to pay by check at a bank a couple blocks away. So everyone (about 100 people) trooped over there at lunch and cashed their check.

Then banks opened “special” checking which required no minimum balance but charged 10c per check.

So if a black–or any other color–woman wanted to open a bank account they would have to be at lease middle middle class. We were lower middle class.

In Quebec, until 1964, it was quite different. A woman had to have a legal guardian, either husband or father or other male relative. The wife of a friend tried to order some furniture (this was after 1964, but the company was still operating under the old rules). The friend had to sign the contract twice, once to give his wife’s permission to sign and once to cosign.

Today, as it happens, is the 87th anniversary of a decision by the Canadian supreme court that a woman was actually a person under the law. Quebec obviously ignored this decision.

Of all the discriminatory practices I’ve heard or read about, I don’t recall reading about white people not wanting to handle money that may have been handled by blacks. I assume when everything is the same green, nobody cares.

Of course, the “logic” of discrimination was truly bizarre. People who wouldn’t eat in the same restaurant as a black person had no problem eating food prepared or served by black people… ??

That seems perfectly logical to me. It’s not about germs, it’s about the “proper social order” of the world. Eating in the same place as them puts them on the same level as you. Them cooking the food does not. Victorian people a house full of servants didn’t eat with them, either. Eating at the same restaurant is too close to socializing with them.

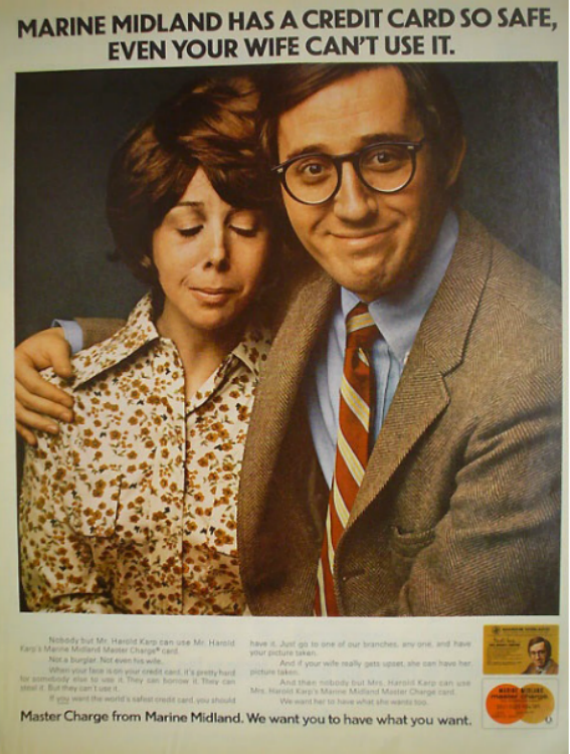

Here is a bank ad from about 1970, advertising a credit card “so safe, even your wife can’t use it.”

{kind=link}

The rubric I heard was that down south, they didn’t care how close you got, as long as you didn’t rise too high, whereas up north, they didn’t care how high you rose, as long as you didn’t get too close.

Presumably, some where in there they also removed the husbands liability for all debts entered into by his wife.

Account operating instructions are a different kettle of fish. Your spouse cannot operate an account that’s yours today unless you permit them to (and the Bank policy allows it). Presumably, your father was the only one using the account until he got married.

In the same way it’s very common even today for to require a co-signer for a loan when you are young, no matter how much you earn; if you have no credit history. Again, were they asking for a con-signer for a woman simply because she was a woman or because she had no credit history?

I do suspect some situations like this have been heard and interpreted by people as meaning “women were unable to do xyz”.

It was in both names; the officer just refused to discuss the account with Mom.

In Texas, in the 50’s, my divorced mother had to get her father to co-sign for a loan on her car.

However, as a city employee she had her own bank account from the 40’s on. She’s beyond asking about this now, she can barely remember last week and sometimes yesterday, but as a child growing up I don’t remember her ever complaining about needing her father’s signature for anything other than the car loan.

This may have been because she belonged to a credit union, which at the time were very distinct from banks. Their mission was to serve teachers and 90% of teachers were female. It would have been silly for the credit union to tell its female depositors they had to have their husband’s signature to open an account.

We’ve gone full circle. After an interval in which every person in America was free to open a bank account (among other things) on sight, it is being reclosed, and banks re prohibited by law from opening an account without presenting certain documentation, which is not necessarily available to all person who may have a need for banking. Banks use their own discretionary power to lock out people of a certain “class”, but some of that selection is mandated by statute.

My bank, for example, has a 30 day waiting period for anyone opening an account who has not been a resident of the state for one year.

I just stumbled across some information that’s relevant. It’s from Winifred Gallagher’s How the Post Office Created America.

The PSS ran from 1911 to 1966, falling off rapidly after WWII. At its peak it held $3.4 billion in deposits.

Here’s an article on it from the USPS historian.

And go back a little further and race was specified!