Chase’s title was also Chief Justice of the United States; he wasn’t just an Associate Justice of SCOTUS. More importantly for the sake of money, he was Secretary of the Treasury during the Civil War and introduced the first “greenbacks,” or Federal currency.

He also got it wrong about the Mint: “which I assume is the fancy crosshatching and whatnot that keeps engravers working day and night on those U.S. Mint printing presses.”

And few people would probably have given you more than three cents for any of them when they were actually in circulation.

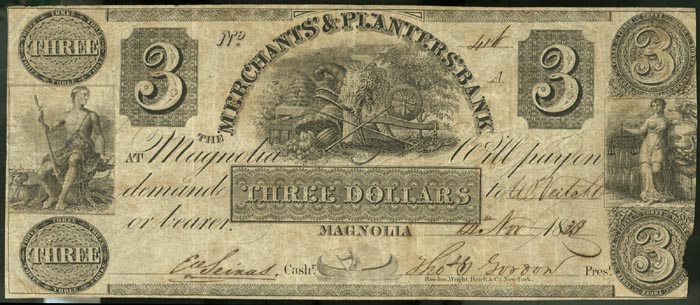

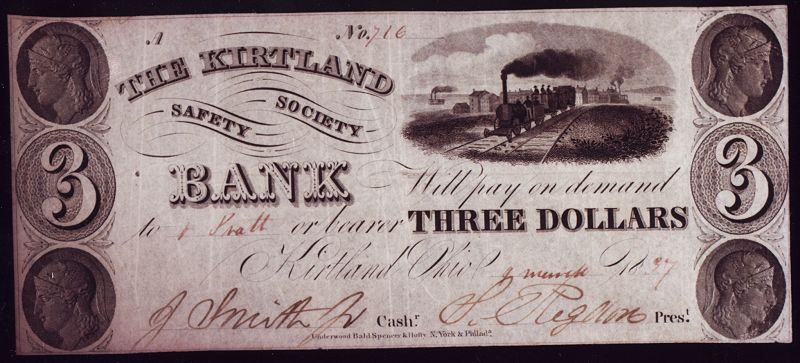

These are the infamous banks notes that floated around when the U.S. had no national bank between 1832 and 1863. Before the Civil War, the U.S. printed no currency. Everything was gold, silver, or some other metal coin. The biggest valued coin was the $20 Double Eagle. Pennies were bigger than quarters since they were made out of 100% copper and had to be big enough to be worth a penny (The small cent piece didn’t come around until the mid-1850s). Carrying around a bunch of coins was hard work, and paying a few hundred dollars for a horse (or let’s face it, a slave) would have required a heavy bag of coins.

Thus, thousands upon thousands of banks produced bank notes. These were paper bills that were back by the full faith and credit of the bank that issued them and were in theory redeemable for coin at that bank. This is the period known as the “Wildcat Banking Period”, so you can imagine what type of banks stood behind the vast majority of bank notes.

The actual value of the bills depended upon the distance to the bank and how trusted the bank was. There were massive books where you could look up the bank note from the individual bank, and how to ascertain it was a legitimate bill. For example, if you were in St. Louis, the Merchant Bank and Tackle Shop of Muddy Creek, Arkansas may go for 30 cents on the dollar. While in Little Rock, it might go for 60 cents on the dollar (or maybe 20 cents because these people were familiar with that bank.)

State banks produced these $3 bills, and the U.S. government never did. The phrase Phony as a three-dollar bill became popular in the 1940s implying that something or someone was not genuine. Later, Strange as a three dollar bill developed to first describe someone who was not quite right, and later to imply the person was a homosexual. In the 1960s and 1970s, this later became Queer as a three dollar bill.

Private bank notes in the US lasted well into the 20th century. They still have them in Scotland. As a legal technicality, they still exist in the US—the Federal Reserve Banks, after all, are banks.

So out of interest, I followed through some of the older postings, and eventually wound up here: treasury.gov

and gosh, multi-billion dollar organisation, and they can’t get better authors to write their website?

That’s not from different sections of the page: it’s just the jumble at the buttom where some tired/bored contractor/civil servant was trying to finish off, and hoping no-one would notice.

And it’s been that way since (at least) January 2011. Text that (obviously) Coca-Cola or Pepsi would be ashamed of, but also Cecil, or even most posters on the SDMB.

The Federal Reserve Banks aren’t banks in the sense they take deposits. It’s a bank for banks. The Federal Reserve Banks were set up in 1913 to loan money to banks experiencing bank runs and to guarantee the honoring of checks. This was due to the 1907 panic which caused a bank run and probably would have created an economic crisis bigger than the Great Depression if J.P. Morgan didn’t personally intervene.

All nationally chartered banks are required to join the Federal Reserve Bank of their region. The banks select a board for their regional Federal Reserve. The 12 regional bank boards are overseen by the seven member board of governors. These members of the board of governors have a 14 year staggered term and the president appoints two every year. The Board of Governors implement policy which is carried out by the regional banks. In the end, the Federal Reserve System acts like a national bank.

After 1862 all state bank notes were taxed at 2% of their face value which pretty much drove them out of circulation. By the beginning of 1863, they no longer exist.

You’re right bank names did appear on some U.S. Currency until 1933. These were called National Bank Notes. However, unlike the earlier state bank notes, National Bank notes were not issued by the banks against their deposits. These notes were a loophole to get out of the limit Congress had placed a limit on the amount of currency the U.S. Treasury could produce. These United States Notes existed until 1971 and were backed by U.S. bonds.

To get around the Congressional limit, the federal government permitted national banks to deposit treasury bonds with the treasury, then the banks could produce currency at 90% of the value of the US debt held by the treasury. These notes, unlike the state bank notes were guaranteed by the U.S. government. Even if the bank failed, the notes were still redeemable by the U.S. Treasury.

The notes said "This note is secured by bonds of the United States deposited in the US treasury in Washington. Then said “The (name of bank) will pay on demand (the amount of note) in cash.” Which meant gold and silver, and after 1900, just gold. These were not printed by the banks, but by the Treasury department and later the Bureau of Printing and Engraving. They had a unified design.

The National Bank Note program was stopped in 1933 since the Federal Reserve Bank could handle the currency issues. By 1971, United States Notes were removed from circulation and the 1861 statue that created them was withdrawn about 20 year later.

As to who was on what bill, it depends on when it was issued. What the article was probably talking about were the federal reserve/US notes; and gold and silver certificates issued after 1925, when the size was reduced to what it is now.

For instance, a hundred years ago, Lincoln was NOT on the five, but Jackson was. Jackson was on the ten in the '20s and didn’t appear on the twenty until 1928, before that Cleveland was. John Marshall was on the five hundred and Alexander Hamilton was on the thousand.

Designs remained static for the most part from 1928 to the 1990s.

Michael Hillegas, first treasurer of The U.S., was on the ten (gold certificates only) on and off all the way until 1930. My favorite is the $5 “educational note” from 1896, with full frontal nudity on the obverse.

{kind=link}

{kind=link}

{kind=link}