This dynamic has been around for decades. What was so special about the bubble years? You keep saying I’m ignoring the roots of the problem and largely pointing to stuff that started in the 1970’s.

There were a lot of natural market forces that were driving this bubble and some government action steered some of those market forces to propel this bubble but the largest role the government played is in what it DIDN’T do.

It would be nice if we knew this stat.

It’s hilarious that the right are trying to blame the 30 year old CRA for the meltdown. Before the meltdown they were criticising the CRA for making loans more expensive due to all the government standards and regulation. Here’s the Cato Foundation in 2003:

But if we look back at the 2003 edition of the Handbook (PDF) we can see that the pre-crisis critique of the CRA was totally different:

There is evidence, however, that the CRA has had at least four negative effects on the communities that it seeks to help. …

Finally, by increasing the costs to banks of doing business in distressed communities, the CRA makes banks likely to deny credit to marginal borrowers that would qualify for credit if costs were not so high. Chief among those costs is the hundreds of millions of dollars in CRA loans that community activists obtain from banks to give their approval of bank mergers and other bank expansions of activities, in an exercise that can be characterized as legalized extortion.

By this logic the CRA should have made the crisis less severe by constraining credit for less creditworthy people!

Now some actual facts :

Firstly, subprime was only a small fraction of the housing bubble. And loans covered by trhe CRA were only a small fration of subprime loans, six percent to be exact :

Recently, Federal Reserve staff has undertaken more specific analysis focusing on the potential relationship between the CRA and the current subprime crisis. This analysis was performed for the purpose of assessing claims that the CRA was a principal cause of the current mortgage market difficulties. For this analysis, the staff examined lending activity covering the period that corresponds to the height of the subprime boom.4

The research focused on two basic questions. First, we asked what share of originations for subprime loans is related to the CRA. The potential role of the CRA in the subprime crisis could either be large or small, depending on the answer to this question. We found that the loans that are the focus of the CRA represent a very small portion of the subprime lending market, casting considerable doubt on the potential contribution that the law could have made to the subprime mortgage crisis.

Second, we asked how CRA-related subprime loans performed relative to other loans. Once again, the potential role of the CRA could be large or small, depending on the answer to this question. We found that delinquency rates were high in all neighborhood income groups, and that CRA-related subprime loans performed in a comparable manner to other subprime loans; as such, differences in performance between CRA-related subprime lending and other subprime lending cannot lie at the root of recent market turmoil.

In analyzing the available data, we focused on two distinct metrics: loan origination activity and loan performance. With respect to the first question concerning loan originations, we wanted to know which types of lending institutions made higher-priced loans, to whom those loans were made, and in what types of neighborhoods the loans were extended.5 This analysis allowed us to determine what fraction of subprime lending could be related to the CRA.

Our analysis of the loan data found that about 60 percent of higher-priced loan originations went to middle- or higher-income borrowers or neighborhoods. Such borrowers are not the populations targeted by the CRA. In addition, more than 20 percent of the higher-priced loans were extended to lower-income borrowers or borrowers in lower-income areas by independent nonbank institutions–that is, institutions not covered by the CRA.6

Putting together these facts provides a striking result: Only 6 percent of all the higher-priced loans were extended by CRA-covered lenders to lower-income borrowers or neighborhoods in their CRA assessment areas, the local geographies that are the primary focus for CRA evaluation purposes. This result undermines the assertion by critics of the potential for a substantial role for the CRA in the subprime crisis. In other words, the very small share of all higher-priced loan originations that can reasonably be attributed to the CRA makes it hard to imagine how this law could have contributed in any meaningful way to the current subprime crisis.

You can also read this, from a Wall Streeter who wrote a book about the meltdown :

This guy has puit a $100 000 challenge up to anyone from the righty think tanks to debate him on whether the CRA/Fannie/Freddie were the cause of the meltdown. He’s still waiting for somebody to take him up on his offer.

Here’s the John Carney guy taken to task :

http://blogs.reuters.com/felix-salmon/2009/06/25/john-carneys-bizarre-crusade-against-the-cra/

And here’s the facts on F anf F :

Federal Reserve Board data show that:

[ul]

[li] More than 84 percent of the subprime mortgages in 2006 were issued by private lending institutions.[/li][li] Private firms made nearly 83 percent of the subprime loans to low- and moderate-income borrowers that year.[/li][li] Only one of the top 25 subprime lenders in 2006 was directly subject to the housing law that’s being lambasted by conservative critics.[/li][/ul]

The “turmoil in financial markets clearly was triggered by a dramatic weakening of underwriting standards for U.S. subprime mortgages, beginning in late 2004 and extending into 2007,” the President’s Working Group on Financial Markets reported Friday.

Between 2004 and 2006, when subprime lending was exploding, Fannie and Freddie went from holding a high of 48 percent of the subprime loans that were sold into the secondary market to holding about 24 percent, according to data from Inside Mortgage Finance, a specialty publication. One reason is that Fannie and Freddie were subject to tougher standards than many of the unregulated players in the private sector who weakened lending standards, most of whom have gone bankrupt or are now in deep trouble.

During those same explosive three years, private investment banks — not Fannie and Freddie — dominated the mortgage loans that were packaged and sold into the secondary mortgage market. In 2005 and 2006, the private sector securitized almost two thirds of all U.S. mortgages, supplanting Fannie and Freddie, according to a number of specialty publications that track this data.

In 1999, the year many critics charge that the Clinton administration pressured Fannie and Freddie, the private sector sold into the secondary market just 18 percent of all mortgages.

Fueled by low interest rates and cheap credit, home prices between 2001 and 2007 galloped beyond anything ever seen, and that fueled demand for mortgage-backed securities, the technical term for mortgages that are sold to a company, usually an investment bank, which then pools and sells them into the secondary mortgage market.

About 70 percent of all U.S. mortgages are in this secondary mortgage market, according to the Federal Reserve.

Conservative critics also blame the subprime lending mess on the Community Reinvestment Act, a 31-year-old law aimed at freeing credit for underserved neighborhoods.

Congress created the CRA in 1977 to reverse years of redlining and other restrictive banking practices that locked the poor, and especially minorities, out of homeownership and the tax breaks and wealth creation it affords. The CRA requires federally regulated and insured financial institutions to show that they’re lending and investing in their communities.

Conservative columnist Charles Krauthammer wrote recently that while the goal of the CRA was admirable, “it led to tremendous pressure on Fannie Mae and Freddie Mac — who in turn pressured banks and other lenders — to extend mortgages to people who were borrowing over their heads. That’s called subprime lending. It lies at the root of our current calamity.”

Fannie and Freddie, however, didn’t pressure lenders to sell them more loans; they struggled to keep pace with their private sector competitors. In fact, their regulator, the Office of Federal Housing Enterprise Oversight, imposed new restrictions in 2006 that led to Fannie and Freddie losing even more market share in the booming subprime market.

What’s more, only commercial banks and thrifts must follow CRA rules. The investment banks don’t, nor did the now-bankrupt non-bank lenders such as New Century Financial Corp. and Ameriquest that underwrote most of the subprime loans.

These private non-bank lenders enjoyed a regulatory gap, allowing them to be regulated by 50 different state banking supervisors instead of the federal government. And mortgage brokers, who also weren’t subject to federal regulation or the CRA, originated most of the subprime loans.

In a speech last March, Janet Yellen, the president of the Federal Reserve Bank of San Francisco, debunked the notion that the push for affordable housing created today’s problems.

“Most of the loans made by depository institutions examined under the CRA have not been higher-priced loans,” she said. “The CRA has increased the volume of responsible lending to low- and moderate-income households.”

In a book on the sub-prime lending collapse published in June 2007, the late Federal Reserve Governor Ed Gramlich wrote that only one-third of all CRA loans had interest rates high enough to be considered sub-prime and that to the pleasant surprise of commercial banks there were low default rates. Banks that participated in CRA lending had found, he wrote, “that this new lending is good business.”

http://www.mcclatchydc.com/2008/10/12/53802/private-sector-loans-not-fannie.html

But at that meeting, Mr. Mozilo, a butcher’s son who had almost single-handedly built Countrywide into a financial powerhouse, threatened to upend their partnership unless Fannie started buying Countrywide’s riskier loans.

Mr. Mozilo, who did not return telephone calls seeking comment, told Mr. Mudd that Countrywide had other options. For example, Wall Street had recently jumped into the market for risky mortgages. Firms like Bear Stearns, Lehman Brothers and Goldman Sachs had started bundling home loans and selling them to investors — bypassing Fannie and dealing with Countrywide directly.

“You’re becoming irrelevant,” Mr. Mozilo told Mr. Mudd, according to two people with knowledge of the meeting who requested anonymity because the talks were confidential. In the previous year, Fannie had already lost 56 percent of its loan-reselling business to Wall Street and other competitors.

“You need us more than we need you,” Mr. Mozilo said, “and if you don’t take these loans, you’ll find you can lose much more.”

Really?!? Going back alllll the way to the mid 90’s is too far? Oh, maybe if you don’t want to look into the issue any further then it is too far. As I’ve stated the CRA was a minor thing from its creation until the Clinton administration demanded that banks show actual numbers of loans in the communities in order to get a great CRA score. For some reason this is meaningless to you. Things can and do change over time. The CRA was not static legislatively or with respect to regulation and enforcement.

I don’t know. In the end it doesn’t matter. Fannie and Freddie were reaching their affordable-housing goals, put in place by HUD, by buying subprime loans from banks regardless of the CRA status of the loans.

See my first comment…and try to think a little.

You asked for a cite for my statement. I provided you with a cite. Maybe you don’t see a link between forcing the GSEs to buy loans from lower income people, subprime loans, and the CRA but that doesn’t mean there is no link.

The GSEs used their own definitions for subprime which significantly understated their exposure to these loans. The Alt-A category has a lot of subprime characteristics. Fannie and Freddie did not list the total number of loans made by people with FICO scores less than 660…which alone would be enough to consider the loan subprime. Also, the loss rates from what fannie and freddie label subprime are almost identical to the the loss rates from the Alt-A loans. So, 40% of Fannie’s loans and 52% of Freddie’s loans between 2005-2007 were junk loans.

You just can’t help yourself. You want to blame the greedy capitalists but you’ll still blame the government if you can pin the blame on the eevul republicans.

Maybe not for the GSEs. See my statement above.

And the GSEs lowered their standards significantly. I thought you knew this by now.

I’m not going to spoon-feed you. It’s a three-page WaPo article. If you can’t be bothered to read THAT little then why bother asking for a cite?

I said you are living in the past if you believe Fannie and Freddie had conforming standards that they imposed on the industry. I stand by that statement. In theory, you are correct but in actuality I am correct. HUD instructed the GSEs not to buy mortgages that did not meet HUDs criteria but the GSEs kept buying these junk loans anyway.

So, anyone who disagrees with you must be parroting Armey? Truly a pathetic statement coming from someone who does not have a handle on the facts to start off with. Who exactly are you parroting? I’ll take a guess and say Barney Frank.

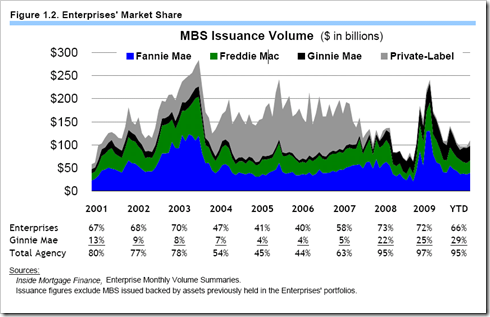

Just to back up the Fannie and Freddie points I made earler, the F and F Conservators’ report on the whole thing was just released. Here’s a picture that paints 100 words :

Look at all that grey. What happened in 2003 that allowed the huge expansion of privately issued mortgae issuance at the expense of F and F?

Here’s a late 2003 presser, another 1000 words. At least :

The guy on the left holding the chainsaw to the stack of mortgage and banking regulations was the Bush-appointed head of one of the US financial regulatory authorities. The one that regulated AIG amongst other firms. In his previous life he was a banking lobbyist who spent his career lobbying congress to lift restrictions on baks, to “cut red tape”, before Bush appointed him to run a regulator in a cunning fox/henhouse move. A move that worked out really well for America.

Here’s a better picture with a much clearer image of the chainsaw/tree shears :

I definitely agree!

[QUOTE=Damuri Ajashi]

I know one appraiser and he basically admitted that his profession had abandoned their principles when he saw 40 year old homes being appraised for more than it would have cost to build new.

[/QUOTE]

WORD!

I was a licensed Appraiser in the mid 90’s early 2000’s. What I saw was enough to make me abandon the field.

Yes I saw “good” honest appraisers;I was one! I also saw VERY many “number hitters”, appraisers that could and would “hit” a mortgage brokers needed number. I also saw home owners that would refi at every given chance sometimes yearly, taking every cent of equity and then some.

An appraisal is the property of the client, in a mortgage transaction the client is typically the broker or bank. There were/are MANY appraisers that will “sell their soul” for the almighty dollar. They can/did get away with it because there is/was very little enforcement of state/federal regulations.

I simply would not play the game…I would NOT cherry pick comparable sales, ignore condition and differed maintenance or over value amenities and up grades.

Since I would not “hit” the number I lost work to the brokers that just wanted to “make the deal”.

My family is still in Real Estate appraisal…they mostly do REO, Bank and Homeowner appraisals.

ymmv,

tsfr

I don’t know if large down payments should be required. I mean, I understand the argument being made, but I don’t know that the benefits of negative equity don’t outweigh the risks.

My wife and I bought our house 9 years ago with 0% down. It was a special program Bank of America was offering for teachers (my wife was a HS teacher). We had to put up some earnest money, but we negotiated to have the sellers pay most closing costs so when we signed the mortgage we actually received a check for several hundred dollars.

Now, we had (and have) excellent credit, and we both worked and were pre-approved for a mortgage almost twice as large as the one we took out - in other words, we bought a house we knew we could easily afford. We did have to pay PMI for a few years until our equity exceeded 20% of the home’s value. But it would have taken at least five years or more to save up a 20% down payment, while housing costs were still rising, and we would be continuing to pay rent while our family was growing.

The crazy part was what we were pre-approved for. I think that’s where the lenders messed up. If we had bought a $300,000 house like they said we could, instead of a $150,000 house, we’d have been screwed when my wife quit her job to have kids. So I think most of the blame falls on people who borrowed more than they could afford, and the banks who loaned them the oversized mortgages. I don’t think it can be blamed exclusively on negative equity.

Yes, that is too far. The bubble didn’t build over 10 years and the cahgnes in teh mid 90’s were not significant enough to have driven the bubble the way you seem to think.

You CLEARLY don’t know what you are talking about but you think you do because someone has fed you a perspective on the history of this financial meltdown that conforms with what you would like to believe.

I gave the reasons for this meltdown earlier and this wasn’t from reading articles or listening to politicians, it was from being involved in these deals and talking to bankers about these deals.

The facts whatever they may be, before about 2002 are irrelevant to the bubble. The bubble didn’t form in 2004 because of rule changes ten years earlier. The bubble formed because non-bank lenders like Countrywide suddenly had access to a secondary mortgage market other than Fannie Mae or Freddie Mac because investment banks had figured out how to sell non-agency paper to insurance companies and pension funds. There were all sort of aggravating factors but the big revolution was when ibanks figured out how to make nonagency paper attractive to investors.

It wasn’t the CRA. It wasn’t Fanie Mae or Freddie Mac. It was greed, combined with a laissez faire attitude and a fed reserve chairman (and this is my little CT) who wanted to prove his lifelong devotion to Aynrandianism correct.

You get into a bit of a chicken and egg problem.

It’s true that during the build up, house prices were going up too fast for normal people to save 20%. And because they were going up so fast, it was decided that people didn’t need to save. The 20% would be made up from appreciation.

But, it’s also true that house prices were going up BECAUSE people could get no-equity mortgages.

Think about your example, you didn’t have the down payment because the price of the house was going up 20% per year. Technically speaking, you SHOULDN’T have been able to buy a house. And if you hadn’t, prices wouldn’t have kept going up.

If there had been a 20% down payment requirement (or any requirements for that matter), home sales would have stalled, and prices wouldn’t have continued to rise. And that would have meant that you could have saved.

Also consider that you are by far an exception to the rule. My wife and I were in the same

boat; we wanted to buy in 2006 when all of our friends were getting townhouses. But at the time, houses were so overvalued we couldn’t afford to. Instead of buying, we continued to rent a cheap condo, continued to save, and in 2009 the market crashed. Suddenly we had both the 20% to put down, and houses we wanted were suddenly extremely cheap.

The process I described COULD have happened in 2001-2004, and had their been lending standards it WOULD have happened. It’s the reason why house prices (and foreclosure rates) were so steady over the past 80 years.

The price of the house you wanted was driven up by speculators, buying on easy credit. Just like the stock market in the 1920s.

You CLEARLY don’t know how to argue. Just because you THINK you gave the correct reason for the meltdown, and because you claim to have some inside knowledge that the rest of us do not possess, does not make either of these claims true. You claim to be right just because you think you are right…and the rest of us with an “agenda” need to shut up and accept your authority. Take off the blinders. Usually this type of post is the one right before the cursing and personal insults start

I’m not really into twisting facts to fit my argument but I can argue the facts. I gave THE reasons why the mortgage meltdown occurred. You use some pretty convoluted logic to reach your conclusion that we can blame the CRA, Fannie and Freddie for the mortgage meltdown. The meltdown was not because of FNMA, FHLMC or CRA, it was the securitization of non-agency backed mortgages that triggered the bubble and it was a lack of confidence in THOSE mortgages that caused the crisis. It wasn’t just securitization, FNMA and FHLMC had beens securitizing their mortgage pools for decades without problems and as we have seen the CRA mortages accounted for a TINY fraction of the subprime mortgages in the market, it was the securitization of subprime mortgages by private label mortgage lenders.

I don’t know how many times this has to be explained. I suppose you will never believe it and I can expect a response along the lines of "no it was the CRA and Fannie Mae (Dick Armey told me so).

Oh…I see now! It all makes sense since you have repeated the same thing three times! Since the answer was so basic I’m shocked, SHOCKED, that the mods have not seen fit to move this to General Questions! :rolleyes:

It really slays and confuses me to think that nobody here holds RE Appraisers and Mortgage BROKERS responsible…they reeked hovack on our financial system and still flew under the proverbial RADAR of our banking’s system of 'checks and balances"…

Clean up the system of Home Mortgages and the market will find its own balance.

ymmv,

tsfr